ECN 204 Lecture Notes - Lecture 7: Impaired Asset, Book Value, Income Statement

Document Summary

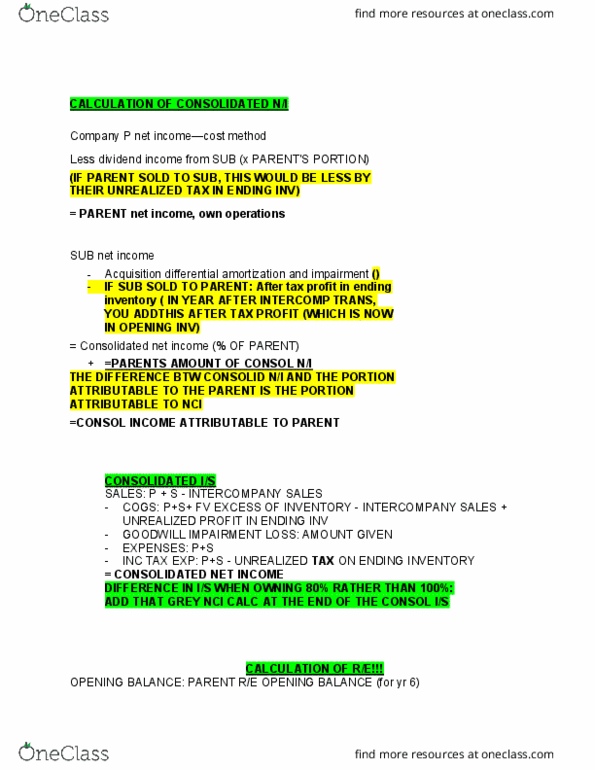

Methods of accounting for an investment in a subsidiary. 2 methods for accounting investment in sub: cost method, entity method. Cost method: acc for investments at cost and income from sub (div) is recorded in net. Income when right to receive inc is established. Equity method initially records at cost, but then adjusts for changes in the investors. Profit/loss of the investor includes their share of the subs profit or loss. Distributions received by the sub reduce the carrying amount of the investment. Adjustments in carrying amount may also come from changes in the parents. The consolidated financial statements must be adjusted to reflect the amortization and/or impairment. In addition to the consolidated f/s, the parent could also prepare non-consolidated f/s. we will refer to these non-consolidated f/s as separate entity financial statements. Dividend income and equity method income from a subsidiary are usually not taxable.