ECN 104 Lecture Notes - Lecture 10: Demand Curve, Profit Maximization, Longrun

3 Mar 2017

School

Department

Course

Professor

Document Summary

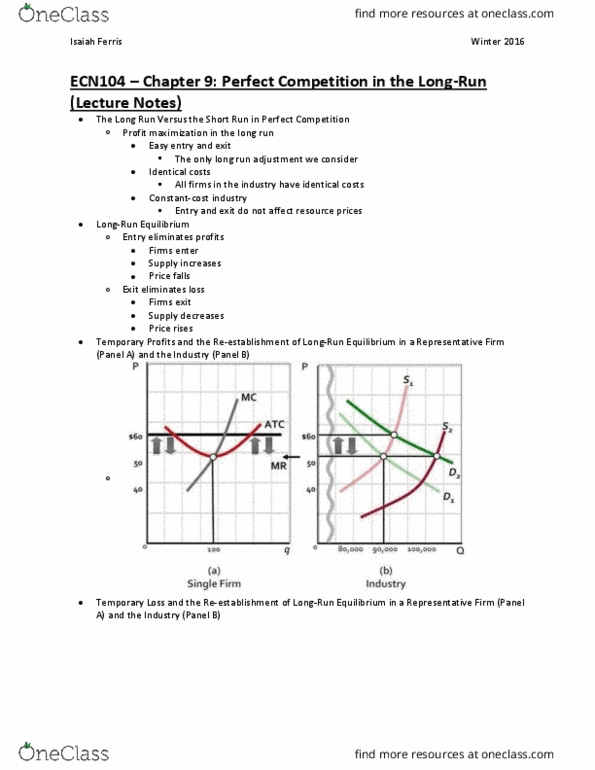

10: the long run versus the short run in perfect competition. The only long run adjustment we consider. All firms in the industry have identical costs: constant-cost industry. Entry and exit do not affect resource prices. Profits attract firms from less profitable industries and losses cause them to leave the unprofitable industry to find another more profitable one. This reflects the supply determinant, a change in the number of sellers. The graphs below show temporary profits and the re-establishment of long-run equilibrium in (a) a representative firm and (b) the industry. A favorable shift in demand (d1 to d2) will upset the original industry equilibrium and produce economic profits. As a result, those profits will entice new firms to enter the industry, increasing supply (s1 to s2) and lowering product price until economic profits are. In other words, an increase in demand temporarily raises price. Temporary profits and the re-establishment of long-run equilibrium in a representative firm and the.