FIN 621 Lecture Notes - Swiss Franc, Money Supply, Purchasing Power Parity

6 Mar 2014

School

Department

Course

Professor

Document Summary

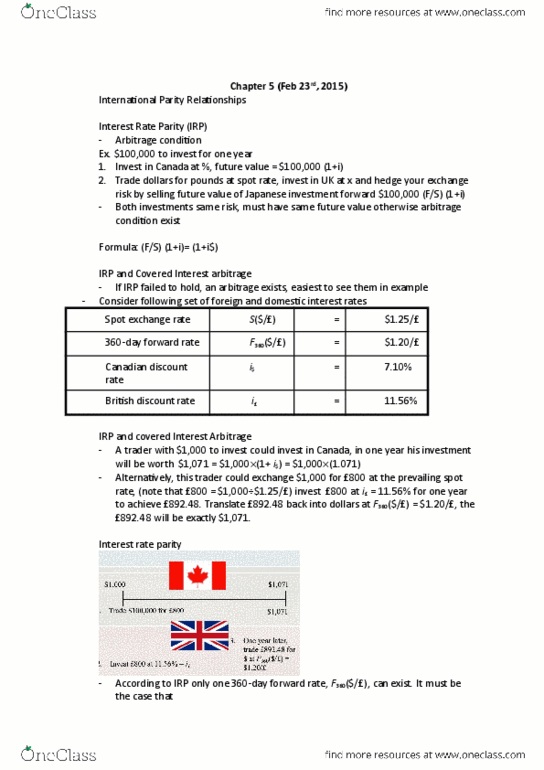

Ibs 621: lecture 3, globalization and the multinational firm, balance of payments, the market for foreign exchange. Fisher effect: using the parity relations in forecasting exchange rates, you observe that spot eur/usd=1. 05, one-year interest rates are: rusd=1. 76%, S spot rate, fc/dc rfc interest rate of foreign currency (fc) rdc interest rate of domestic currency (dc) If irp failed to hold, an arbitrage would exist. It"s easiest to see this in the form of an example. Arbitrage: consider the following set of foreign and domestic interest rates and spot and the case that. If f360($/ ) . 20/ , riskless arbitrage is possible. Sell forward gbp and buy spot gbp to make it riskless: alternative 1 forward exchange rates. Irp and covered interest arbitrage worth ,071 = ,000 (1+ i$) = ,000 (1. 071: alternative 2. Invest ,000 in canada @ ___%, in one year investment will be. Exchange ,000 for 800 at the going spot rate, (note that 800 =