FIN 501 Lecture 12: FIN 501 Chap 12 - Return, Risk, + SML.docx

20 Nov 2014

School

Department

Course

Professor

Document Summary

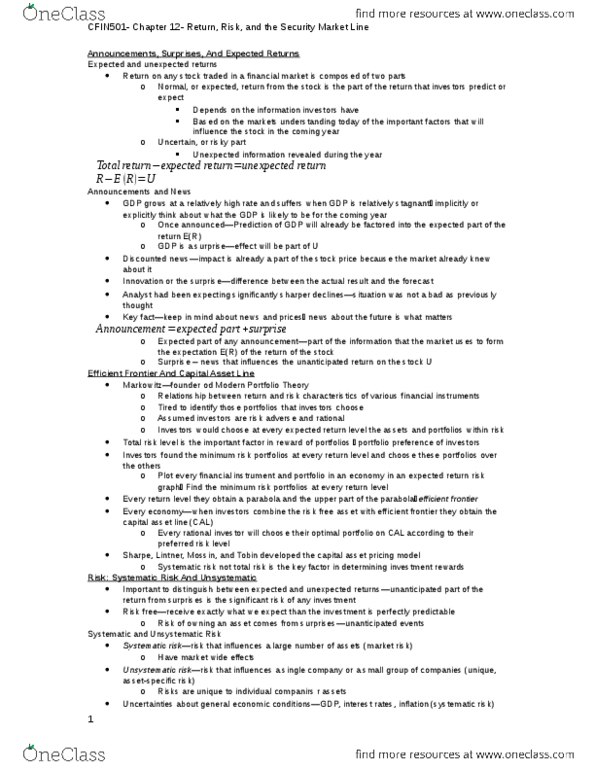

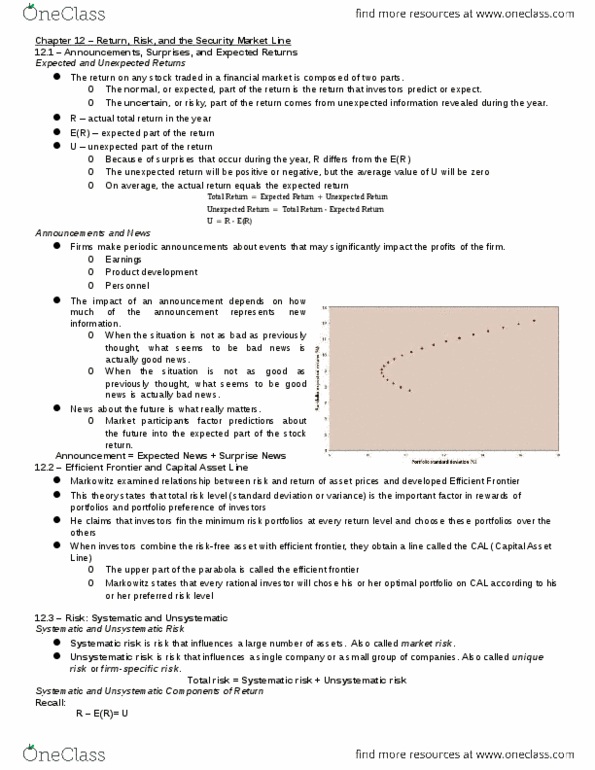

Normal expected part of return that investors predict/expect. Uncertain risky part of return from unexpected info revealed during year. Firms make periodic announcements about events that may significantly impact profits o o o. Impact of announcement depends on how much of it represents new info. Market participants factor predictions about future into expected part of stock return o. Markowitz frontier relationship between risk + return of asset prices. Influences single company or small group of companies. Can diversify aka unique risk or firm-specific risk. R er = u = systematic + unsystematic = m + . Systematic risk principle : reward for bearing risk depends only on systematic. > 1. 0 have more systematic than avg. < 1. 0 have less systematic than avg. Total risk of portfolio has no simple relation to total risk of assets in portfolio. For 2 assets, you need 2 variances + covariance. For 4 assets, you need 4 variances + 6 covariances.