ACC 414 Lecture : Accounting Forms

11 Feb 2013

School

Department

Course

Professor

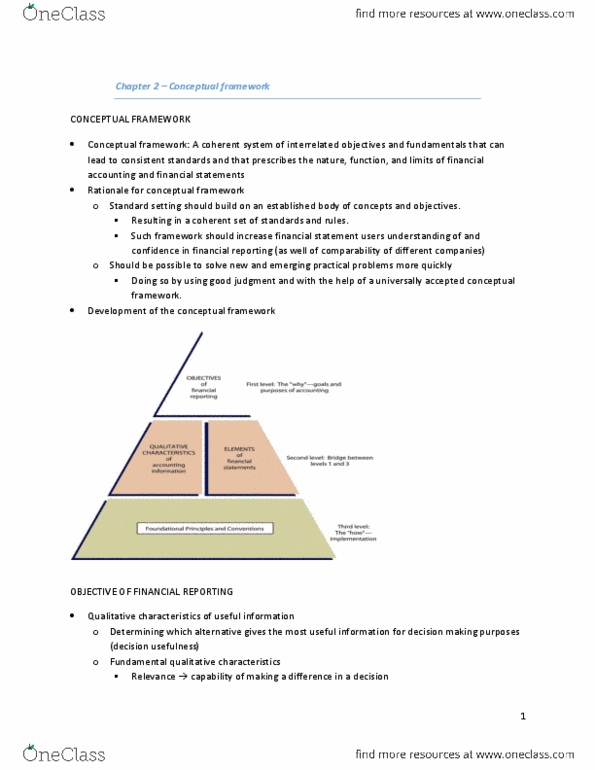

Document Summary

This implies the expression, with clarity, of accounting information in such a way that it will be understandable to users - who are generally assumed to have a reasonable knowledge of business and economic activities. This implies consistent treatment of similar items and application of accounting policies. This implies the ability for users to be able to compare similar companies in the same industry group and to make comparisons of performance over time. Much of the work that goes into setting accounting standards is based around the need for comparability. This implies that the accounting information that is presented is truthful, accurate, complete (nothing significant missed out) and capable of being verified (e. g. by a potential investor). This implies that accounting information is prepared and reported in a neutral way.