ACC 406 Lecture Notes - Lecture 7: Variable Cost, Fixed Cost, Earnings Before Interest And Taxes

16 Oct 2017

School

Department

Course

Professor

Document Summary

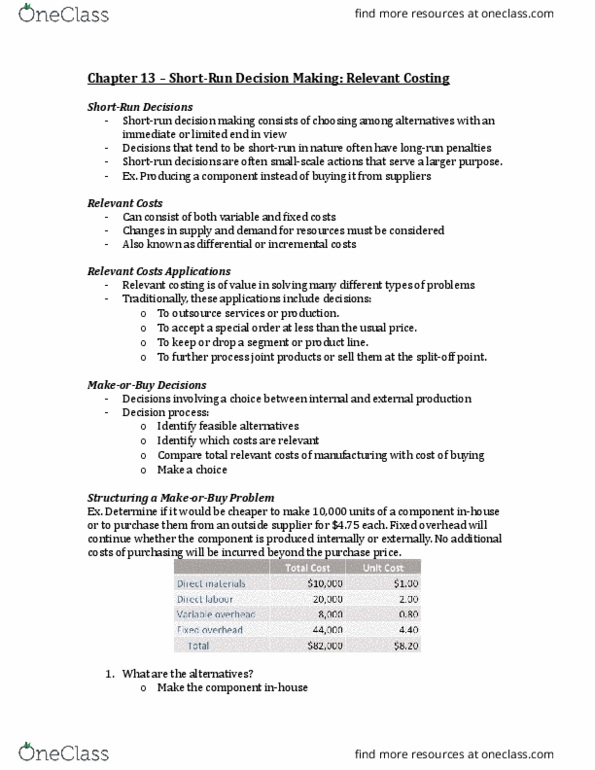

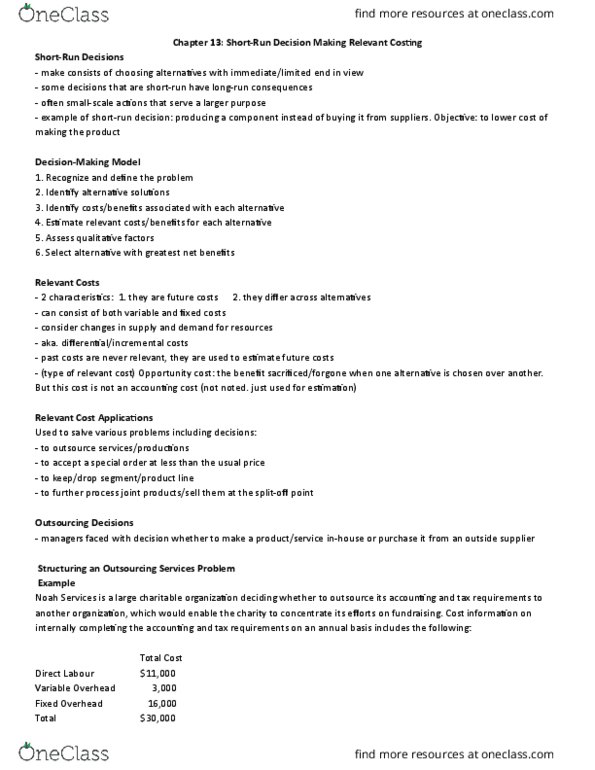

Identify which costs are relevant: compare total relevant costs of manufacturing with cost of buying, make a choice. Determine if it would be cheaper to make 10 000 units of a component or purchase them outside for. Example: keep-or-drop decisions tile has a cm = 10000 (sales of 150000 less total variable cost of 140000 all variable costs are relevant relevant costs associated with this line: advertising =10 000, supervision =35 000. List the alternatives being considered: keep the tile line or drop the tile line. Example: structuring a keep-or-drop product line probem with complementary effects dropping the product line reduces block sales by 10% and brick sales by 8% all the other information remains the same. 8 machines provide 40 000 machine hours per year. X; unit cm of , requires 2 hours of machine time. Y; unit cm of , requires 0. 5 horus of machine time.