ECON 1B03 Lecture Notes - Lecture 21: Perfect Competition, Form 10-Q, Natural Monopoly

22 Mar 2016

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

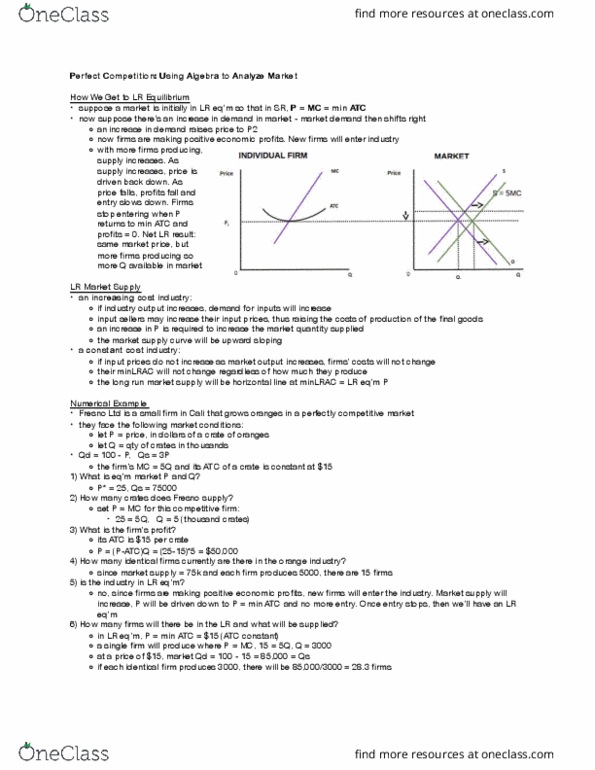

Derive irms lr supply curve produces p = mc, when p > min atc. Will shut down if p < min atc , quanity = 0 ie the green y axis. The sum of quaniies supplied by individual irms in market. For any given price, each irm makes p = mc. Supply curve relects irms marginal cost curves big aggregate mc curve. P=mc = min atc (zero economic proit) there is increase in demand product, the demand shits right ind equilibrium price, green area is at new higher price, is posiive proit. More irms producing and entering, supply shits right, so price drops. Entry stops when p returns to min atc and proits =0, net lr result is the same market price but more irms producing more q in market. Increasing cost industry if industry output increases, demand for inputs increases. Input seller may increase input prices thus raising cost of producion of inal good.