COMMERCE 2FA3 Lecture Notes - Lecture 3: Systematic Risk, Loanable Funds, Risk Premium

10 Apr 2017

School

Department

Course

Professor

Document Summary

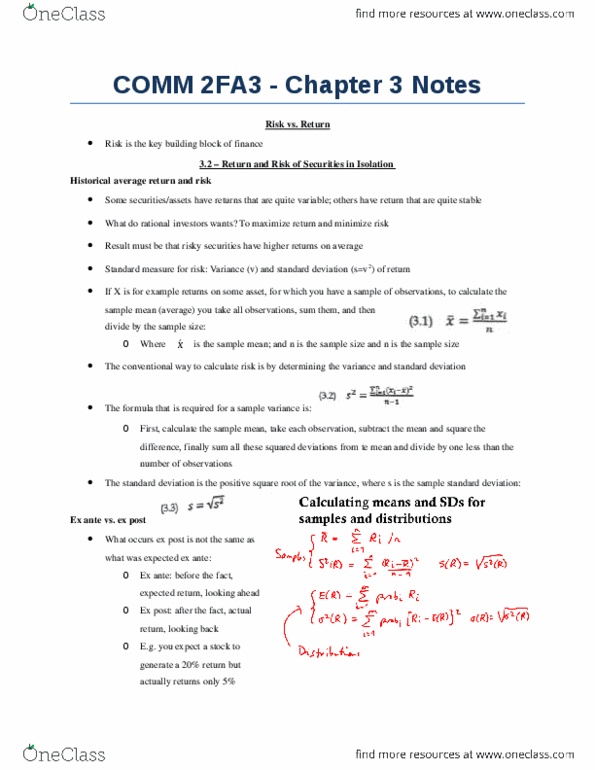

L3 chapter 3 rewarding nerve & 4. 4 hedging. 3. 1 how is risk measured? (sd and beta) Risk is measured using variance and standard deviation ( . Sd of a stock reflects its risk if held in isolation. Securities > stocks, securities could be grouped together in portfolios. Correlation: the correlation between random variables x and y. o o o. Portfolio theory: portfolio returns are simply weighted averages of the returns on all securities making up the portfolio o. The return of the portfolio, x is the weight of the securities x is the weight of securities. o. Diversification: risk can be reduced without surrendering any return. Wise investors will not hold a single security but rather a portfolio of securities. There are a lot of numbers of ways of combining them into portfolios of securities. o. The variance of the portfolio (portfolio risk): o. As you increase the number of securities in your portfolio: