COMMERCE 2AB3 Lecture 2: Manufacturing Company Costs

11 Jan 2018

School

Department

Course

Professor

Document Summary

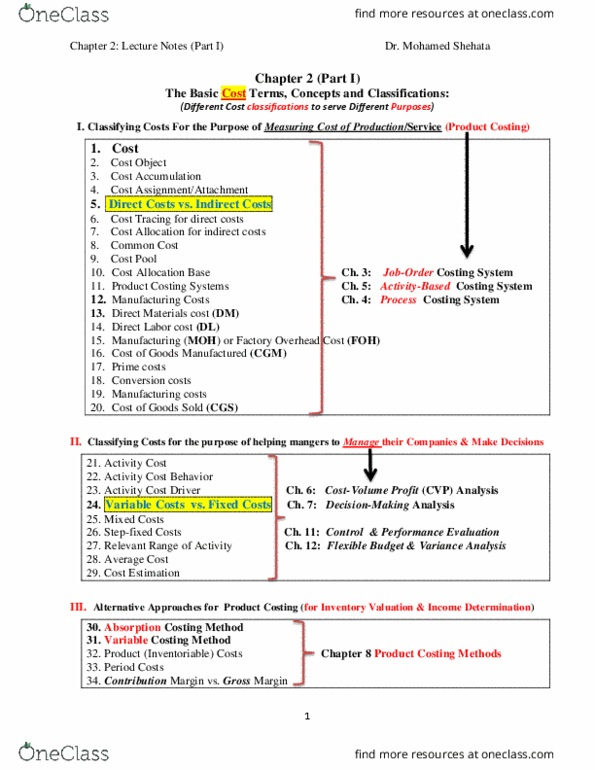

Having different cost classifications to serve (achieve) different purposes (objectives) Product costing ( calculating the cost of production) Decision making (planning, directing & controlling), to help managers make decisions. Manufacturing companies engage in a series of activities to develop, design, produce and market a product. These activities can be summarized in the value chain. Each step increases the value of the product to the customers, and also incurs many costs that needs to be accounted for. Costs are incurred inside the factory to produce/create/invent the product (manufacturing. Costs are also incurred before production begins or after production ends (non-manufacturing. Assets - economic resources with future benefits, can be considered to be similar to cost. Cost - the monetary amount that must be paid to acquire and/or use economic resources (such as assets) for the purpose of producing a product ( or performing a service), with the ultimate objective of generating revenues.