COMMERCE 2AB3 Lecture Notes - Lecture 3: Contribution Margin, Earnings Before Interest And Taxes, Income Tax

21 Jan 2017

School

Department

Course

Professor

Document Summary

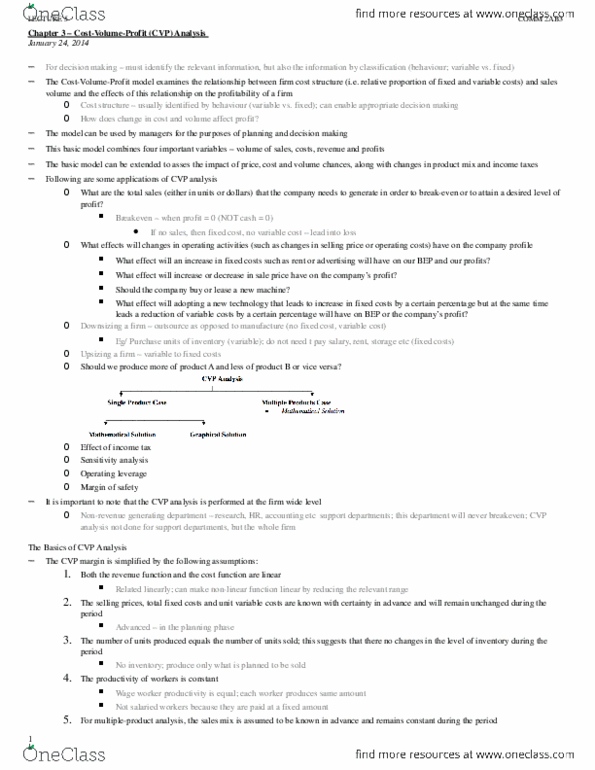

Cvp analysis, income statement, and the contribution margin. Cost-volume-profit (cvp) analysis: the study of the effects that changes in costs a(cid:374)d (cid:448)olu(cid:373)e ha(cid:448)e o(cid:374) a (cid:272)o(cid:373)pa(cid:374)(cid:455)"s profits, analysis important in profit planning, critical factor in management decisions. Setting selling price, determining product mix, and maximizing use of production facilities. Five components of cvp analysis: (1) volume or level of activity. Behavior of both costs and revenues in linear throughout the relevant range of the activity index: (2) unit selling prices. All costs classified, with reasonable accuracy, as either variable or fixed: (3) variable cost per unit. Changes in activity (volume) are the only factors that affect costs: (4) total fixed costs. Inventory levels remain constant all units produced are sold: (5) sales mix. Sales mix is constant when more than one type of product is sold. Percentage of total sales that each product represents will stay. If assumptions are not valid, results of cvp analysis may be inaccurate the same.