COMMERCE 1AA3 Lecture Notes - Lecture 4: Going Concern, Common Stock, Financial Statement

15 Sep 2016

School

Department

Course

Professor

Document Summary

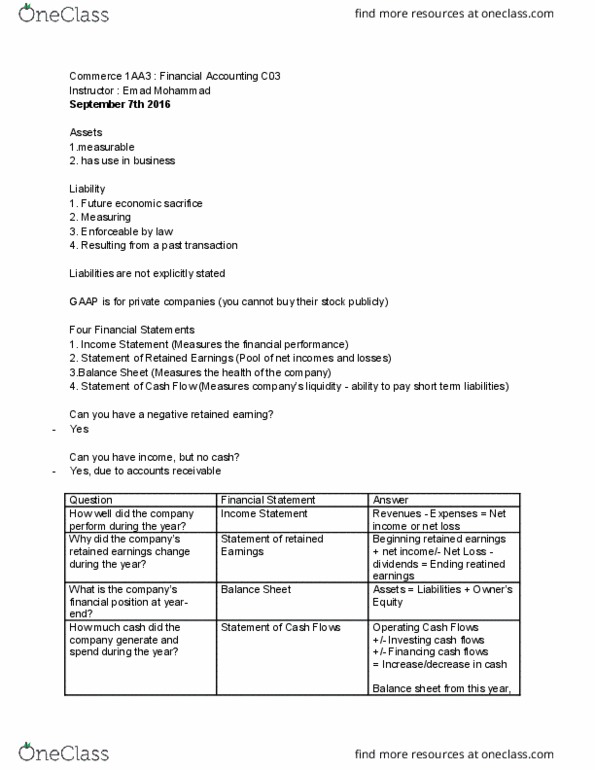

Equity - represents the stockholder"s ownership of the business. Financing (paying dividends, shares, long term liabilities, borrowing money, paying off loan) Not all the money in the company bank is owned by the company, some of it could be part of a uncashed cheque. The rest of the slides in chapter one should be read, and is mostly self explanatory. Income statement (last line: retained earnings, cash flow statement (first line, all of the above, only a and b above. Relevant (predictive value, able to be verified) Full disclosure of information (there are some exceptions: complete, neutral/free of bias, free from error. To obtain the above, the below must be put into consideration. Assumption: unit of measurement should stay the same o. *separate entity - the business is a person, and should not be mixed up with the owner"s personal affairs: periodicity, going concern - assume that the company will continue to operate.