COMMERCE 1AA3 Lecture Notes - Lecture 5: Cash Flow Statement, Current Liability, Current Asset

6 Mar 2017

School

Department

Course

Professor

Document Summary

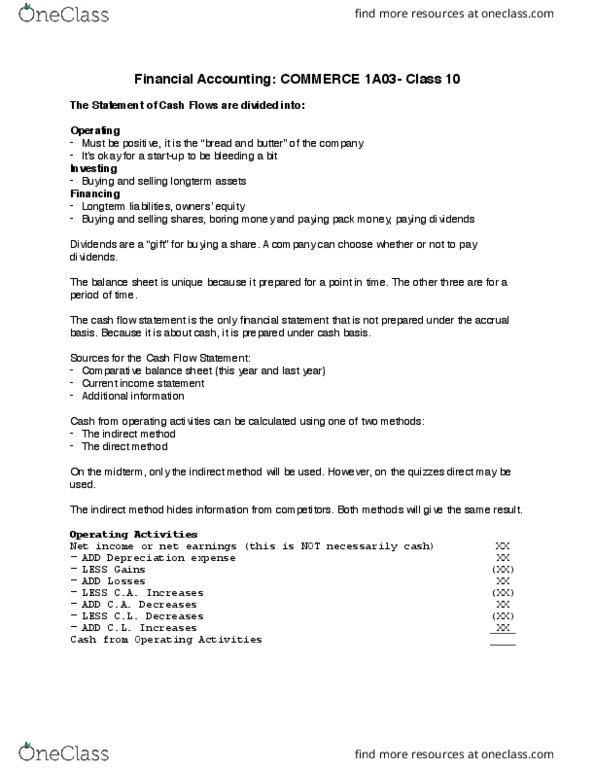

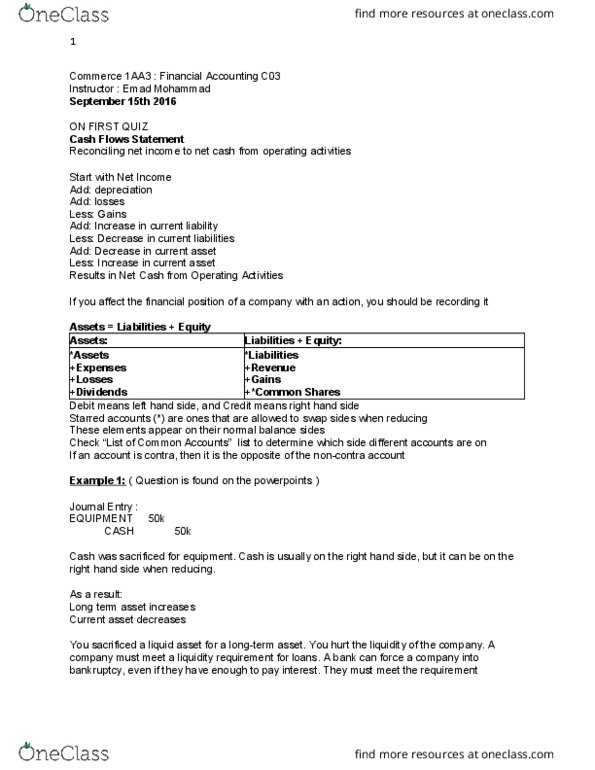

Act. xx xx (xx) xx xx (xx) (xx) xx xx. Asset + expenses + losses + dividends = liabilities + revenues + gains + common shares. They are allowed to swap sides when reducing. Debit vs credit are not about good vs bad. The way they appear is called normal balance. Remember slide 10 in chapter 2 for the names of all accounts. If you buy k of equipment with cash, this is what the t account should look like: If you provide k worth of service, and the customer pays 2k in cash, 1k on credit. A journal entry shows a change (gives the change, not the total of an account). A t-account keeps a running total, unlike a journal entry. Trial balances start with current asset, then the longterm asset, then current liability, then longterm liabilities, then expenses. Net income is an estimate/opinion because you don"t know how much a company will really make by the very end.