MGCR 293 Lecture Notes - Demand Curve, Economic Equilibrium, Marginal Cost

21 Nov 2012

School

Department

Course

Professor

Document Summary

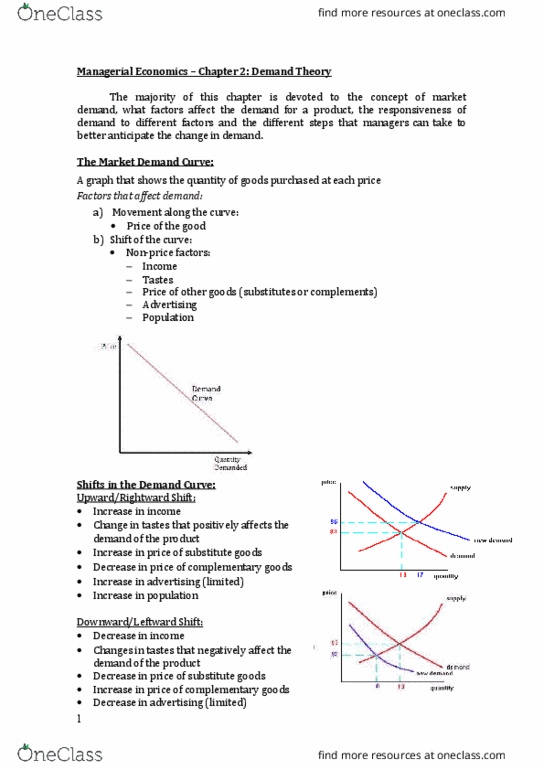

Shift in demand any of non-price determinants change (e. g. income, tastes & preferences, population, expectations, price of related goods, etc. : whole curve shifts right or leftward. Increase in demand means the curve shifts rightward, or an increase in quantity demanded at every price. Different from change in quantity demanded: a change in a good"s own price leads to a change in quantity demanded a move along the same demand curve. Law of supply: the price of a product or service and the quantity supplied are directly related. As price goes up, the quantity supplied increases, and vice versa. Market supply schedule: sharing a list of possible products, prices, and corresponding quantities supplied by all firms. Non-price determinants: cost of inputs (capital, land, labour), technology & productivity, taxes & subsidies, number of firms in the industry, price expectations. Change in supply vs. change in quantity supplied refer to demand. Price at which quantity demanded of a product equals the quantity supplied.