MGCR 211 Lecture Notes - Lecture 16: Subledger, General Ledger, Accrual

9 Feb 2018

School

Department

Course

Professor

Document Summary

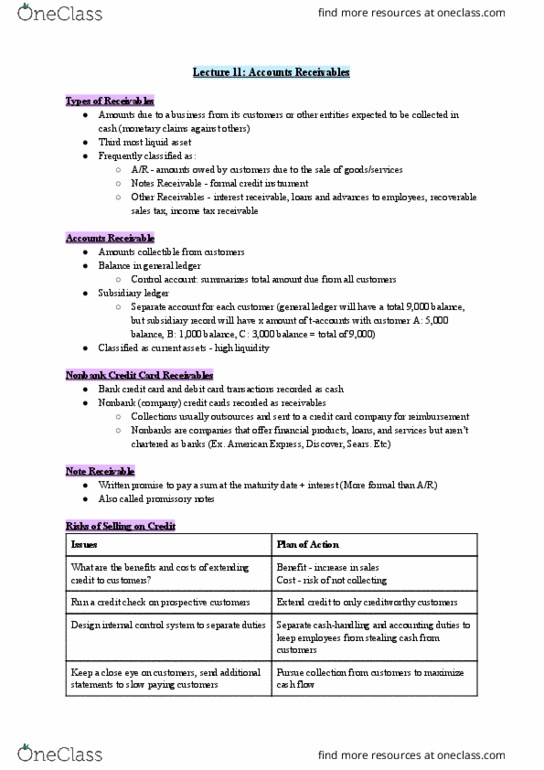

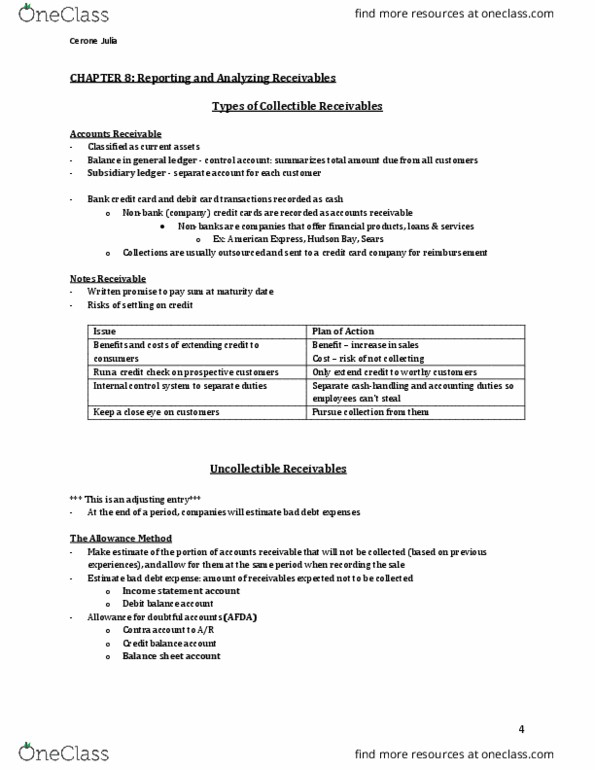

Chapter 8 - reporting and analyzing receivables (1/11/16) Subsidiary ledgers : a group of accounts that share a common characteristic (eg. they"re all receivable accounts, to record each customer that owes them money so they can keep track of the balance owed by any. 1 interest revenue: when interest revenue is recognized/accrued, the interest amount for the specific period is calculated, then debited to interest receivable, and credited in interest revenue. 2 comparing notes: notes receivable = notes payable, except one is an asset and the other a. Payable liability: the maker records it as a payable, and the payee records it as a receivable. Derecognizing notes receivable : principal amount of note receivable and its interest is collected when due, then removed/ derecognized from the books. Income statement : bad debts expense - an operating expense, interest revenue is reported in the non-operating section.