ACCT 475 Lecture 11: ACCT 475 – Lecture 11

16 Jan 2018

School

Department

Course

Professor

Document Summary

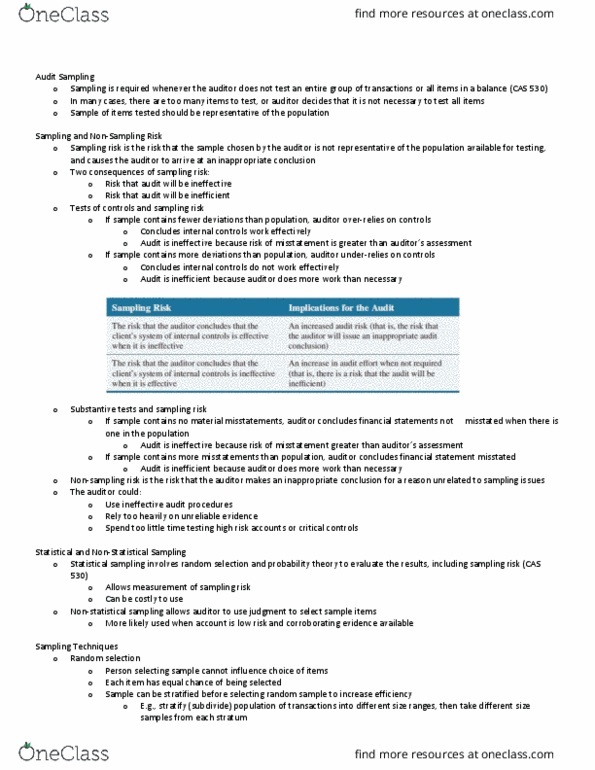

Chapter 6: sampling and overview of the risk response phase of the. Sampling is required whenever the auditor does not test an entire group of transactions or all items in a balance (cas 530) In many cases, there are too many items to test, or auditor decides that it is not necessary to test all items. Sample of items tested should be representative of the population. Examples: medical sampling blood sample (don"t drain your entire blood stream!) In terms of controls (do they work or not work?) correct. In some cases you don"t need to sample if your client has only 6 customers (6 a/r), test all 6! In you were auditing a bank with thousands of loans from customers then it makes sense to take a sample. Sampling risk is the risk that the sample chosen by the auditor is not representative of the population available for testing, and causes the auditor to arrive at an inappropriate conclusion.