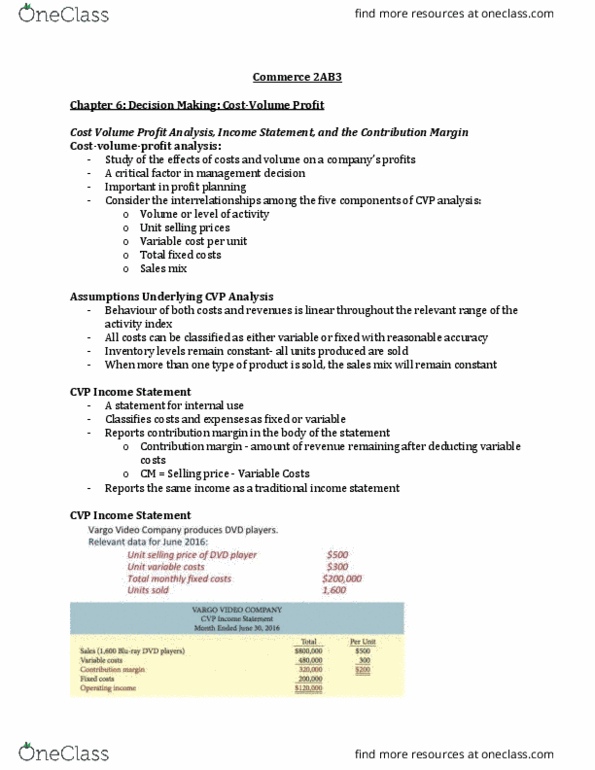

ACCT 361 Lecture Notes - Lecture 3: Income Statement, Contribution Margin, Procyclical And Countercyclical

Document Summary

Get access

Related Documents

Related Questions

Kiwi Cellars has many competitors in the New Zealand domesticpremium wine market. The wines are judged similarly in quality& taste although KC employs different production and marketingmethods. Dissatisfied with its current profitability, KC managementis considering their competitive options. An accounting departmentanalyst compiled the following data for the most recent year tofacilitate our analysis.

Note: Assume that the company sells what itproduces, thus they do not produce wine to hold over ininventory.

KC | BenchmarkCompetitor | |

Sales price per unit (750 ml bottle) | $8.50 | $8.00 |

Variable materials (grapes, bottles, etc.) per unit | $2.25 | $2.75 |

Variable labor per unit | $1.25 | $2.00 |

Variable production overhead (utilities, etc.) perunit | $1.00 | $1.25 |

Fixed production overhead (depreciation, etc.) | $750,000 | $250,000 |

Marketing, administrative and other fixed costs | $250,000 | $150,000 |

Last yearâs sales in units | 350,000 | 400,000 |

Capacity in units | 500,000 | 450,000 |

1. Demand in recent years has been volatile varying from a lowof 200,000 to a high of 400,000 units. As a measure of the impactof this uncertain demand on profit by assuming demand increases ordecreases by 10%.

Interpret the relative changes in profit.

2. Recommend a coherent plan for how KC could increase profit inthe coming year and calculate the resulting profit for yourplan.

Explain your answer, evaluating their current position relativeto your recommendation.

3. Now assume that the data above for Kiwi actually consists oftwo wines with the following data:

KC-Chard | KC-Shiraz | |

Sales price per unit (750 ml bottle) | $ 7.50 | $ 11.00 |

Variable cost per unit | $ 4.20 | $ 5.25 |

Last yearâs sales in units | 250,000 | 100,000 |

a. Describe the KC's Unit Level Cost-Volume-Profit (CVP)relationship.

b. Describe the Cost Behavior Analysis - by analyzing the KiwiCellar's business problems.

c. What are the concepts underlying cost-volume-profit analysisfor Kiwi Cellars?

d. What can be said about the Breakeven and Profit Planning ofthe company

e. What can you conclude by conducting an Analysis of OperatingLeverage

Overview: Classifying a companyâs costs allows for an in-depthanalysis of the impact that changes in output have on revenues,costs, and net income or net loss. A cost-volume-profit (CVP)analysis will be completed in order to determine the breakevenpoint. Relevant costs will be used to prepare a flexible budget.Additionally, an appropriate costing system should be selected andthe choice should be substantiated with reasonable rationale.Finally, a memo should be prepared for management that summarizesthe results of the quantitative analysis and makes recommendationsfor an optimal costing system to be ethically used by key decisionmakers. For Milestone One, you will use the MDE ManufacturingBudget (Table I) to analyze costs, contribution margin, andbreakeven point for the bird feeder division of the company. In Tab1 of your Student Workbook, classify costs as either product orperiod costs. Briefly explain the difference between the types ofcosts. Then, analyze the actual costs and, using Tab 2 of yourStudent Workbook, complete a cost-volume-profit analysis todetermine how many bird feeders must be sold at the current costand sales price level to earn a 10% profit and how much the salesprice would have to increase to earn a 10% profit at the same costand sales volume level. Submit the Student Workbook with Tabs 1 and2 completed with your cost calculations and a 1â2 page Worddocument that explains the implications of your findings andaddresses all of the critical elements in Section I.

I. Salesand Manufacturing Expenses: Budget and Actual (2014)

You will use this table to complete Milestones One and Two.

Budget ($) | Actual ($) | |

Sales | 1,050,000 | 991,700 |

Expenses | ||

Materials â Cedar | 225,000 | 248,160 |

Materials â Plastic | 37,500 | 37,741 |

Factory Worker Labor | 300,000 | 332,760 |

Materials â Indirect | 3,000 | 2,585 |

Factory Depreciation | 78,000 | 78,000 |

Factory Utilities | 12,000 | 12,000 |

Factory Maintenance and Repairs | 5,000 | 4,500 |

Shipping ($2.25/each) | 112,500 | 105,750 |

Sales Commissions ($2.00/unitsold) | 100,000 | 94,000 |

Office Rent | 12,000 | 12,000 |

Advertising | 20,000 | 20,000 |

Liability insurance | 5,000 | 5,000 |

Office Depreciation | 1,000 | 1,000 |

Office Salaries | 48,000 | 48,000 |

Total Expenses | 959,000 | 1,001,496 |

II. Contribution Margin: Static Budget and Actual Results (2014)

You will use this table to complete Milestone Two.

Actual Results | Static Budget Amount | |

Units Sold | 47,000 | 50,000 |

Revenues ($) | 991,700 | 1,050,000 |

Manufacturing Costs ($) | ||

Variable | 621,246 | 565,500 |

Fixed | 94,500 | 95,000 |

Gross Margin | 275,954 | 389,500 |

| Milestone One,Part I | ||

| Product Costs | ||

| Period Costs | ||

| Totals | Totals | ||||||||||

| Budget | Actual | ||||||||||

| Sales Price per Unit | |||||||||||

| Variable Costs | |||||||||||

| Materials - Cedar | |||||||||||

| Materials - Plastic | |||||||||||

| Factory Worker Labor | |||||||||||

| Materials - Indirect | |||||||||||

| Shipping ($2.25/ea) | |||||||||||

| Sales Commissions ($2/unit sold) | |||||||||||

| Variable Cost per Unit | |||||||||||

| Contribution Margin | |||||||||||

| Fixed Costs | |||||||||||

| Factory Depreciation | |||||||||||

| Factory Utilities | |||||||||||

| Factory Maintenance and Repairs | |||||||||||

| Office Rent | |||||||||||

| Advertising | |||||||||||

| Liability Insurance | |||||||||||

| Office Depreciation | |||||||||||

| Office Salaries | |||||||||||

| Total Fixed Costs | |||||||||||

| Using Budgeted Amounts | |||||||||||

| Breakeven Point - | Breakeven Point - | ||||||||||

| Using Actual Amounts | Units at Current Sales Price | ||||||||||

| + 10,000 profit | |||||||||||

| Using actual amounts | New Contribution Margin | ||||||||||

| + 10,000 profit | Current Variable Costs | ||||||||||

| New Sales Price | |||||||||||