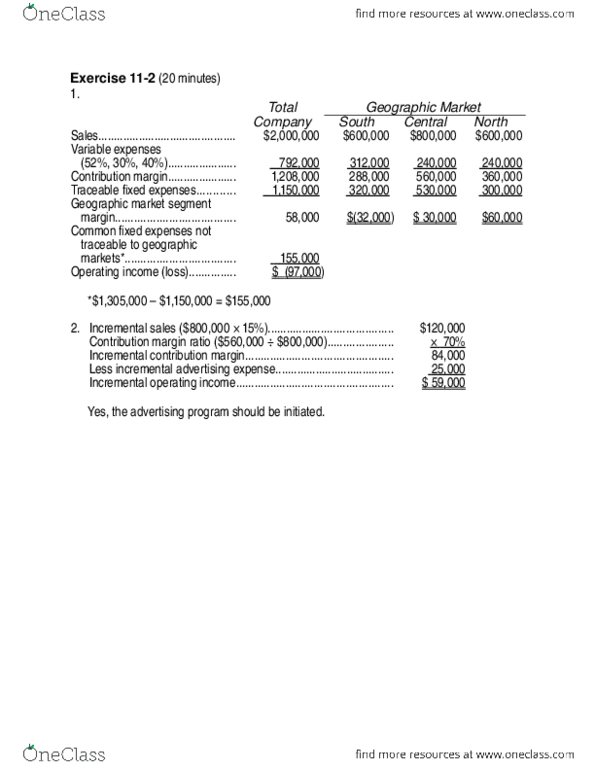

EXERCISE 6-16 Working with a Segmented Income Statement; Break-Even Analysis [L06-4, L06-5]

Raner, Harris, & Chan is a consulting firm that specializes in information systems for medical and

dental clinics. The firm has two offices—one in Chicago and one in Minneapolis. The firm classi-

fies the direct costs of consulting jobs as variable costs. A contribution format segmented income

statement for the company's most recent year is given below:

Sales ........

Variable expenses ..........

Contribution margin ...........................

Traceable fixed expenses .......................

Office segment margin ..............................

Common fixed expenses not traceable to offices .....

Net operating income ......

Total Company

$450,000 100%

225,000 50%

225,000 50%

126,000 28%

99,000 22%

63,000

$ 36,000 8%

Office

Chicago

Minneapolis

$150,000 100% $300,000 100%

45,000 30% 180,000 60%

105,000 70% 120,000 40%

78,000 52% 48,000

$ 27,000 18% $ 72,000 24%

-16%

1496

Required:

1. Compute the company wide break-even point in dollar sales. Also, compute the break-even

point for the Chicago office and for the Minneapolis office. Is the company wide break-

even point greater than, less than or equal to the sum of the Chicago and Minneapolis

break-even points? Why?

By how much would the company's net operating income increase if Minneapolis increased

its sales by $75,000 per year? Assume no change in cost behavior patterns.

3. Refer to the original data. Assume that sales in Chicago increase by $50,000 next year and

that sales in Minneapolis remain unchanged. Assume no change in fixed costs.

a. Prepare a new segmented income statement for the company using the above format.

Show both amounts and percentages.

b. Observe from the income statement you have prepared that the contribution margin ratio

for Chicago has remained unchanged at 70% (the same as in the above data) but that the

segment margin ratio has changed. How do you explain the change in the segment mar-

gin ratio?