FILM-6010 Lecture Notes - Lecture 2: Finance Lease, Operating Lease, Book Value

9 Jun 2020

School

Department

Course

Professor

Tutorial Activities (Week Beginning Monday 16 May):

Part A

TQ.1

a) What is off-balance-sheet financing?

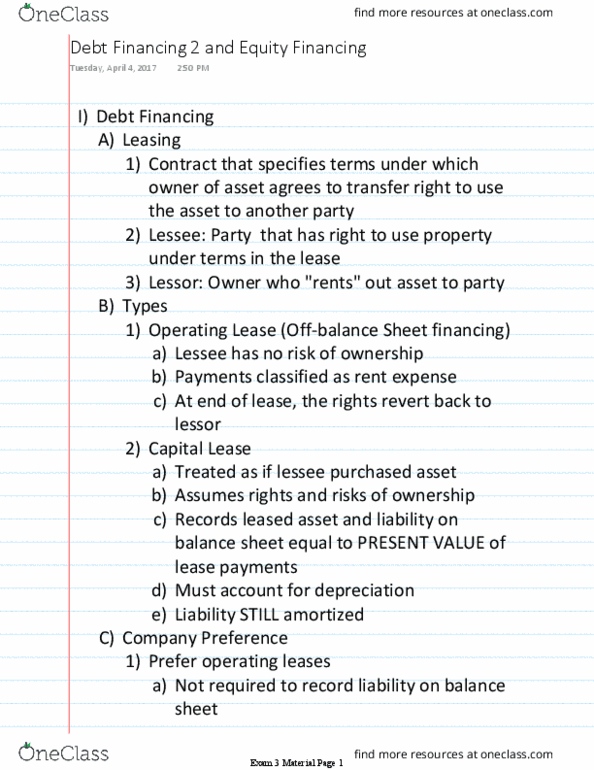

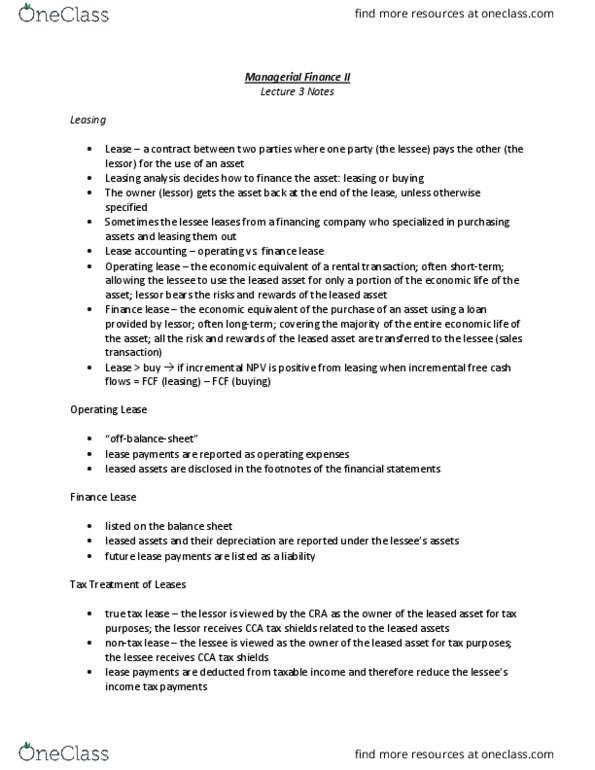

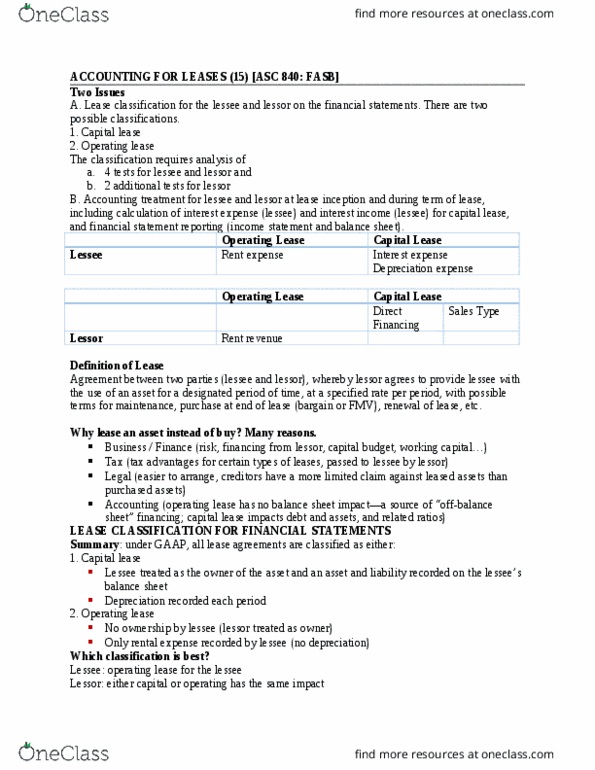

Off-balance sheet financing is when a firm does not include a liability on its balance

sheet. These type of transactions, such as operating leases and partnerships, will

have effect in the debt and liability of a firm.

Borrowing that is not in the balance sheet, could be on the notes

off balance sheet financing is when companies enter into contracts to acquire assets, but such

contracts do not result in an asset or liability being recognized in the balance sheet. An example of

this is operating leases. While a finance lease recognizes an asset (leased asset) and a liability (lease

liability), an operating lease only recognizes a lease expense for the period. Companies can structure

lease contracts so that the terms allow them to classify leases as operating.

b) Tiny Aircraft Airline (TAA) Ltd has total liabilities of $12,000,000 and equity of $6,000,000.

TAA decides to invest in another plane which costs $6,000,000 and has an expected useful life of 30

years, after which it will be ‘mothballed’ in the Mojave Desert. TAA is considering the following

alternatives:

i) Borrow $6,000,000 from the bank and purchase the plane. Loan terms are: 11% interest paid

annually, with principal due after 14 years.

ii) Enter into a 14 year lease with annual lease payments of $800,000 in arrears and a bargain

purchase option of $405,000. The interest rate implicit in the lease is 10%. There are additional

costs of $300,000 in negotiating the lease paid at the beginning of the first year of the lease. If the

lease is classified as a finance lease, this cost is included in the carrying amount of the lease asset.

Compare the immediate effect of purchasing or leasing the plane on TAA’s debt/equity (D/E)

ratio and the effect on depreciation expense (straight-line), interest expense and lease expense,

as applicable, for the first year. For the lease alternative, please consider the effects of

classification as a finance lease and classification as an operating lease in both D/E ratio and

expense calculations. You may ignore taxes.

The immediate effect of purchasing or leasing the plane on TAA’s debt/equity (D/E) ratio,

which indicates how much debt the company is using to finance its assets relative to its equity:

• Purchasing the plane.

After the purchasing of the plane, the debt ratio is 300% (=$18m/$6m).

• Leasing the plane

o Finance Lease

The debt ratio is 300% (=$18m/$6m) because the capitalisation of the leased asset

increases the value of reported non-current assets, and the recognition of the present

value of future lease payments as a liability increases reported current and non-current

liabilities.

o Operating Lease

The debt ratio is 200% (=$12m/$6m) because the amount of the operating lease is

recognised as an expense over the lease term.

The effect on depreciation expense (straight-line), interest expense and lease expense for the first

year:

• Purchasing the plane

Recognition of the interest expenses value as $660,000 per year (= $6,000,000*11%).

Recognition of the depreciation expenses (straight-line) of the plane.

• Leasing the plane

o Finance Lease

▪ Recognise the plane as an asset at the inception of the lease.

▪ Recognise a liability at the inception of the lease. The lease liability is reduced as

the lessee makes lease payments.

▪ Recognise depreciation expenses (straight-line) on the leased asset, this

transaction will affect annual profit over useful life of 30 year.

▪ Recognise interest expenses, which reduces annual profit.

o Operating Lease

▪ Lease payments are recognised as an expense on a straight-line basis over the

lease term.

Borrow

Finance Lease

Operating Lease

D/E ratio

3

2.98

2

Interest Expense

660,000

Lease expense

800,000

Depreciation Expense

200,000

442,382

c) Assume TAA leases the plane. Do you think that the accounting treatment of the lease (i.e.,

whether it is capitalised or expensed) would have any effect on the share price? Give reasons

for your answer.

NO

I think that the accounting treatment, whether it is capitalised or expensed, it will have an effect on

the share price due to the disclosure. According to the EMH, regardless if the information is on the

balance sheet or disclosure in the notes, the share price will reflected the information. Therefore,

the participants (shareholders, new investors, creditors) will read the balance sheet and notes.

If the lease is classified as a finance lease, the information regarding the lease will be directly

presented in the balance sheet. However, if the lease is classified as an operating lease, the relevant

information regarding the lease, its nature and future obligations will be disclosed in the notes to the

financial statements. Under EMH, the share price reflects all publicly available information, not just

information in the balance sheet but information in the notes as well. Therefore the classification of

the lease should not affect the share price provided the same level of information is provided in both

cases.