ECON 203 Lecture Notes - Lecture 4: National Accounts, Factor Cost, Business Cycle

21 Feb 2018

School

Department

Course

Professor

Document Summary

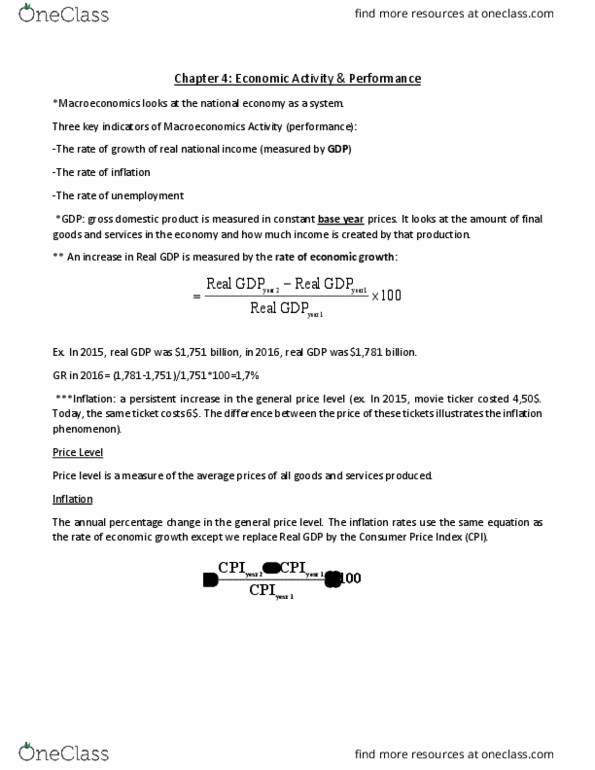

Output: a measure of the total quantity of goods and services produced in the economy. It is also a measure of the incomes generated by that production. Real gdp: the quantity of final goods and services that are produced in the economy in a specific time period. It is the real income in the economy and the quantity of goods and services the economy can afford to buy. Growth in real gdp is necessary to maintain standard of living. The changes that are seen in real gdp are the results of changes in the quantity of goods and services produced and not the result of changing prices. * increased quantities of goods and series provides for an increased standard of living in the economy* Economic growth: defined as an increase in real gdp. Annual rate of economics growth: the annual percentage change in real gdp. Real gdp year 2( current year) - real gdp base year (old year)/ real.