COMM 217 Lecture Notes - Lecture 8: Unemployment Benefits, Savings Account, Working Capital

17 Mar 2018

School

Department

Course

Professor

Document Summary

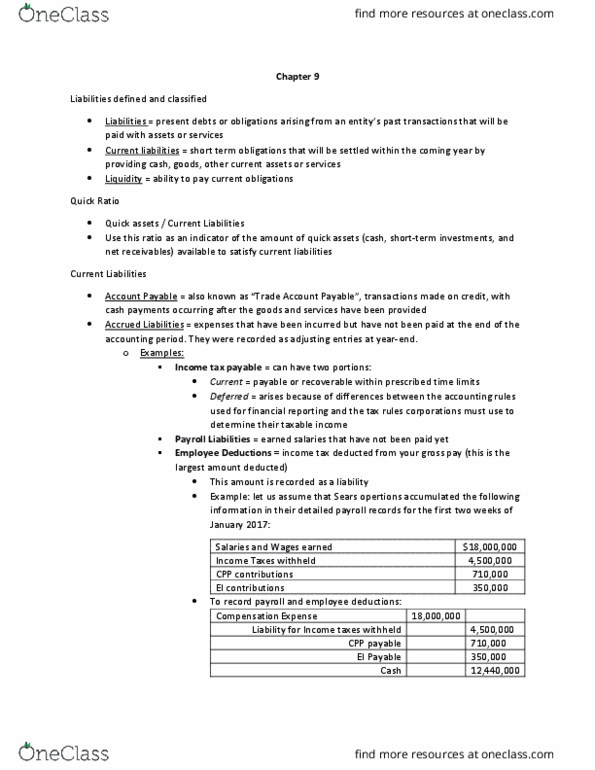

Chapter 9 reporting and interpreting current liabilities. Liabilities: present debts or obligations arising from an entity"s past transactions that will be paid with assets or services. When a liability is first recorded, it is measured in terms of its current cash equivalent, which is the cash amount that a creditor would accept to settle the liability immediately. Current liabilities: short-term obligations that will be settled within the coming year by providing cash, goods, other current assets or services. "does the company currently have the resources to pay its short-term debt?" Quick assets include cash, short-term investments and net receivables. If the exact amounts of the liabilities will not be know with certainty until a future, event, they must be estimated and recorded if they relate to transactions that occurred during the accounting period. Most often, the estimate of (i. e. future warranty costs) is based on a percentage of net sales.