COMM 217 Lecture 5: Chapter 6 - Reporting and Interpreting Sales Revenue, Receivables and Cash

17 Mar 2018

School

Department

Course

Professor

Document Summary

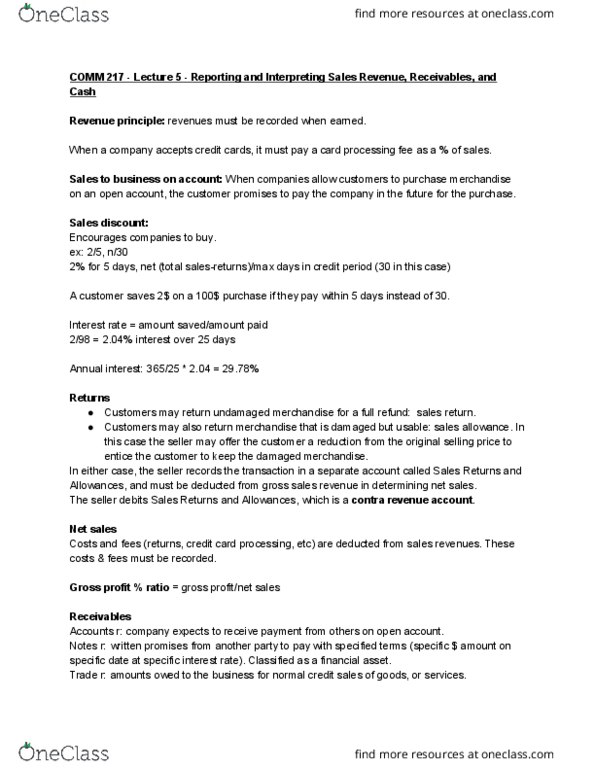

Chapter 6 reporting and interpreting sales revenue, receivables and cash. Contra revenue account: an account that reduces our total revenues on the statement of earnings. 2/10 means that if they pay within 10 days they get a 2% discount. N/30 means that the payment is due within 30 days. A customer returns a product he bought for earlier. How to show (cid:862) ales di(cid:272)ou(cid:374)t(cid:863) a(cid:374)d (cid:862) ales r. &a. (cid:863) a(cid:272)(cid:272)ou(cid:374)ts o(cid:374) the state(cid:373)e(cid:374)t of ear(cid:374)i(cid:374)gs. Bad debt is a necessary risk of selling goods to customers on account. Bad debt accounts for those customers who will not pay their debt off. Bad debt expense is normally classified as a selling expense and is closed at year end. (matching. Two wa(cid:455)s to cal(cid:272)ulate (cid:862)bad de(cid:271)t e(cid:454)pe(cid:374)se(cid:863: percentage of credit sales method. Ex: prior history of the company shows that 1% of credit sales (cid:449)o(cid:374)"t (cid:271)e (cid:272)olle(cid:272)ted. Estimated bad debt = ,000 x 1% = ,000.