ECON 2020 Lecture Notes - Lecture 3: Production Function

14 Sep 2016

School

Department

Course

Professor

Document Summary

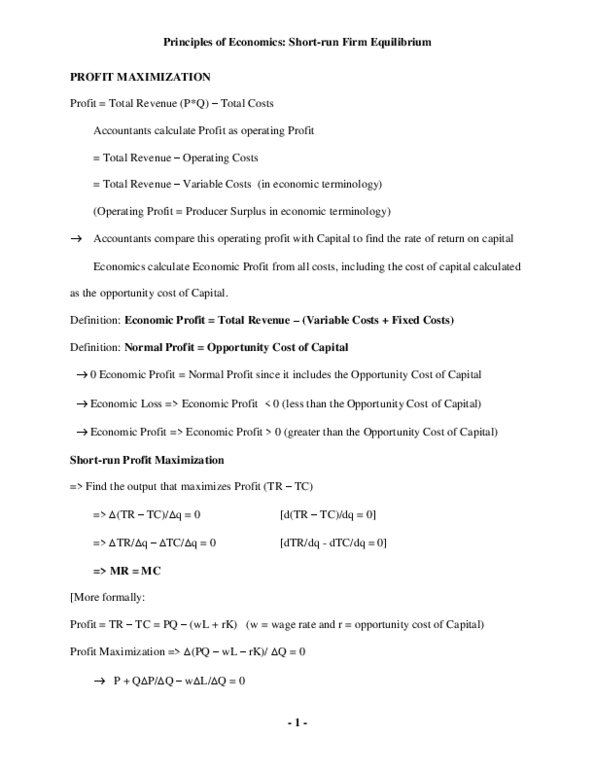

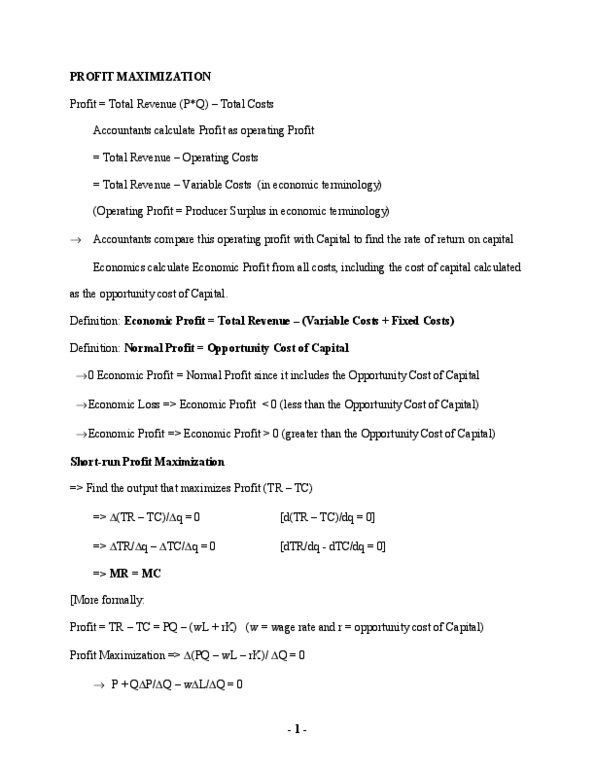

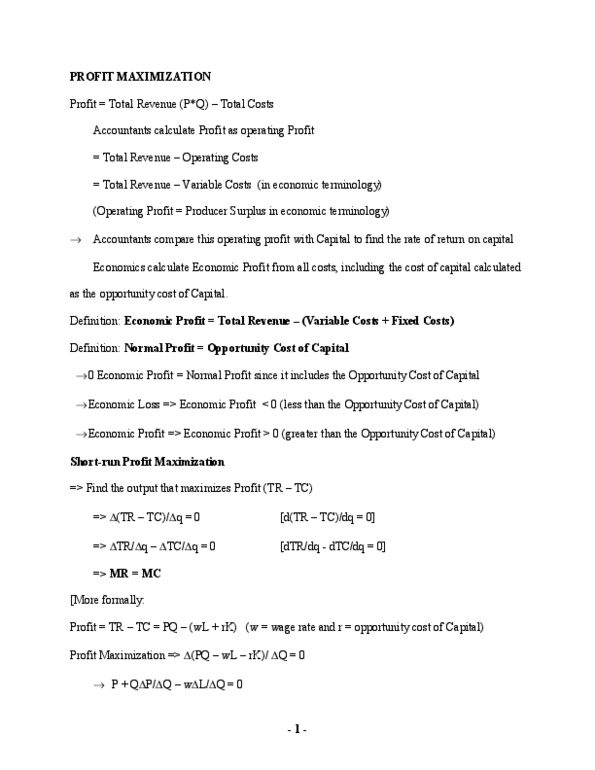

Ultimate objective of firms is to maximize profit: We can express this in two ways: taking the production function approach(ch. 6, taking the cost function approach (ch. 7) 1)profit from producing q units of output is: pi(q) = pq expenditure. Suppose the only input is labour: pi(l) = pf(l) wl, see (fig. 2) 2) profit of producing a q units of output is: pi(q) = pq - cost of 1. Prof likes to give partial credits on marking assignments/homework. The production function: takes inputs, processes them and spits out the quantity of output. Can analyze/study this for short and long run in long run, can be strategic with labour and capital: labour is easier to vary rather than the capital. In the short run, one of the inputs is going to be fixed. Q=f(l,k*: k*, in this case is a constant, cannot be varied. Tp = total product: tp(l) = f(l,k) Ap = average product: ap(l) = (tp(l))/l = (f(l,k*))/l.