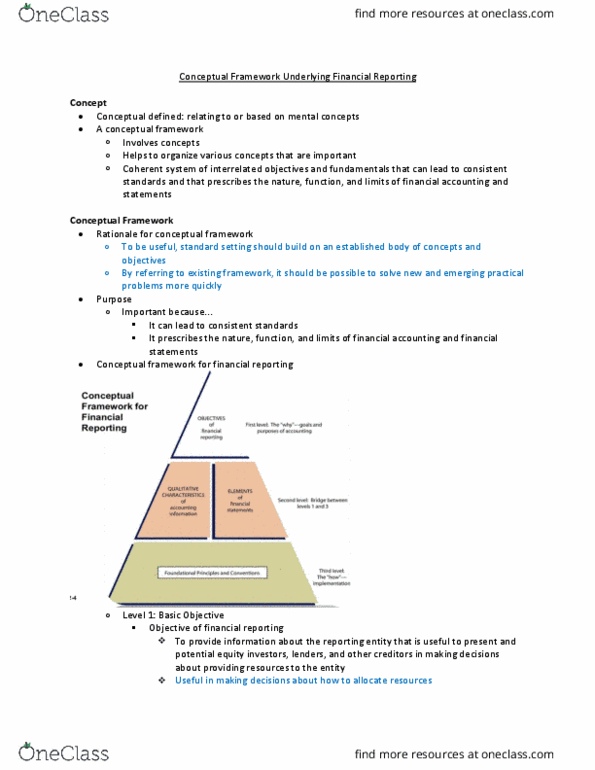

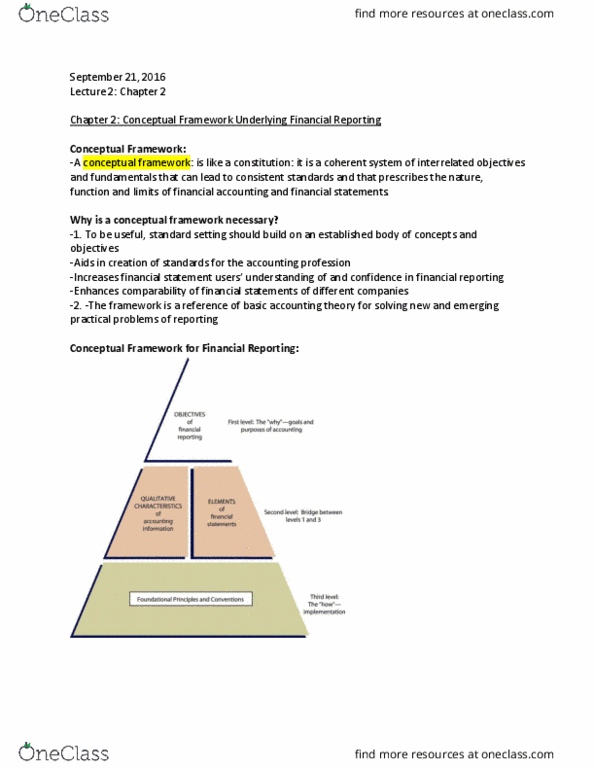

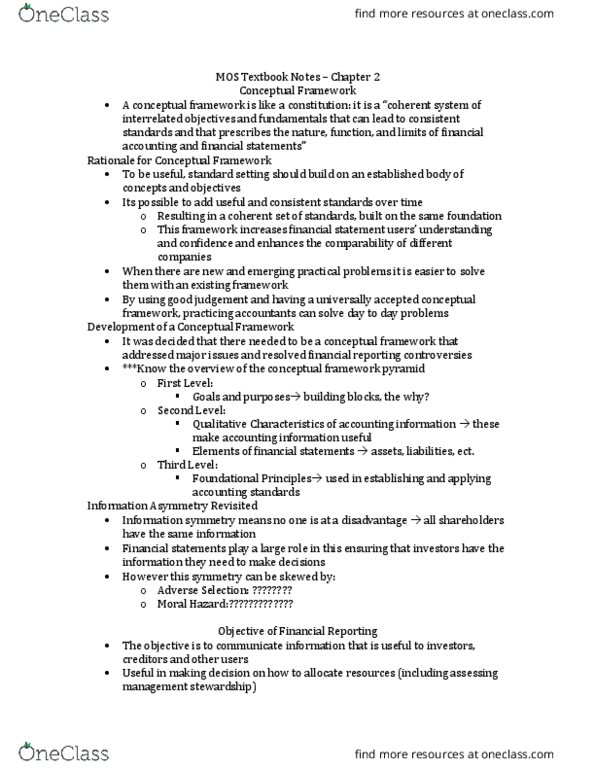

Chapter 2 Conceptual Framework for Financial Reporting LO 2.1Describe the usefulness of a conceptual framework.

A _____________________ in accounting is important becauserule-making should be built on and relate to an established body ofconcepts.

The benefits of a soundly developed conceptual framework are asfollows: a) ______________________________________________________b) ______________________________________________________

Which of the following is not true concerning a conceptualframework in accounting? A. It should be a basis forstandard-setting. B. It should allow practical problems to besolved more quickly by reference to it. C. It should be based onfundamental truths that are derived from the laws of nature. D. Allof these answer choices are true.

LO 2.2 Understand the objective of financial reporting. Toprovide financial information about the reporting entity that is_______________ to present and potential equity_________________________________in making decisions aboutproviding resources to the entity.

In other words the objective is_________________________________________________________________________________________________________________________________________.

LO 2.3 Identify the qualitative characteristics of accountinginformation. The qualitative characteristics of accountinginformation distinguish better and more useful information frominferior and less useful information.

a.Fundamental qualities of useful accounting information.

Relevance._______________________________________________________________________________________________________________________________________________________________

(a)Predictive value.:_____________________________________________________________________________________.

(b)Confirmatory value:_________________________________________________________________________________.

(c)Materiality.:_________________________________________________________________________________.

FaithfulRepresentation.___________________________________________________________________________________________________________________________________________________

(a)Completeness_________________________________________________________

(b)Neutrality_______________________________________________________

(c)Free from error___________________________________________________

b.Enhancing Qualities Enhancing qualities complement thefundamental qualities and include:

Comparability__________________________________________________________________.

Consistency_____________________________________________________________________________________________________________________ Verifiability__________________________________________________________________.

Timeliness__________________________________________________________________.Understandabili_____________________________________________________________________________________________________________________

Select the qualitative characteristics for the followingstatements.

(a) Quality of information that assures users that informationrepresents the economic phenomena that it purports torepresent.

(b) Information about an economic phenomenon that corrects pastor present expectations based on previous evaluations.

(c) The extent to which information is accurate in representingthe economic substance of a transaction.

(d) Includes all the information that is necessary for afaithful representation of the economic phenomena that it purportsto represent.

(e) Quality of information that allows users to comprehend itsmeaning.

SFAC No. 8 identifies the qualitative characteristics that makeaccounting information useful. Presented below are a number ofquestions related to these qualitative characteristics andunderlying constraint.

(a) What is the quality of information that enables users toconfirm or correct prior expectations?

(b) Identify the pervasive constraint developed in theconceptual framework.

(c) The chairman of the SEC at one time noted, âIf it becomesaccepted or expected that accounting principles are determined ormodified in order to secure purposes other than economicmeasurement, we assume a grave risk that confidence in thecredibility of our financial information system will beundermined.â Which qualitative characteristic of accountinginformation should ensure that such a situation will not occur? (Donot use faithful representation.)

(d) Muruyama Corp. switches from FIFO to averagecost to FIFOover a 2-year period. Which qualitative characteristic ofaccounting information is not followed?

(e) Assume that the profession permits the savings and loanindustry to defer losses on investments it sells because immediaterecognition of the loss may have adverse economic consequences onthe industry. Which qualitative characteristic of accountinginformation is not followed? (Do not use relevance or faithfulrepresentation.)

(f) What are the two fundamental qualities that make accountinginformation useful for decisionmaking?

(g) Watteau Inc. does not issue its first-quarter report untilafter the second quarterâs results are reported. Which qualitativecharacteristic of accounting is not followed? (Do not userelevance.)

(h) Predictive value is an ingredient of which of the twofundamental qualities that make accounting information useful fordecision-making purposes?

(i) Duggan, Inc. is the only company in its industry todepreciate its plant assets on a straight-line basis. Whichqualitative characteristic of accounting information may not befollowed?

(j) Roddick Company has attempted to determine the replacementcost of its inventory. Three different appraisers arrive atsubstantially different amounts for this value. The president,nevertheless, decides to report the middle value for externalreporting purposes. Which qualitative characteristic of informationis lacking in these data? (Do not use relevance or faithfulrepresentation.)

If the LIFO inventory method was used last period, it should beused for the current and following periods because of A.consistency. B. verifiability. C. materiality. D. timeliness.

According to the FASB's conceptual framework, what does theconcept of faithful representation include? A. Predictive value B.Materiality C. Verifiability D. Neutrality

Which of the following is not a basic assumption underlying thefinancial accounting structure? A. Going concern assumption B.Economic entity assumption C. Historical cost assumption D.Periodicity assumption

Under current GAAP, inflation is ignored in accounting due tothe A. periodicity assumption. B. economic entity assumption. C.going concern assumption. D. monetary unit assumption.

Valuing assets at liquidation values rather than cost isinconsistent with the A. historical cost principle. B. materialityconstraint. C. periodicity assumption. D. expense recognitionprinciple.