ACCT3321 Lecture Notes - Lecture 10: Risk Measure, Operating Cash Flow, Horizon Problem

CHAPTER 9 – RANKIN

Earnings Management

- Enron scandal

Importance of Earnings

- Sometimes called the bottom line or net income

- Indicates to users the extent to which an entity has engaged in activities that add

value to it the theoretical value of an entity’s stock is the present value of its future

earnings

- Increase = an increase in entity value

- Decrease = decrease in entity value

- Earnings are used by shareholders to assess manager’s performance and to assist in

predicting future cash flows and assessing risk

- Lenders use earnings as a component in debt covenants to reduce the risk associated

with lending and to monitor performance against covenants

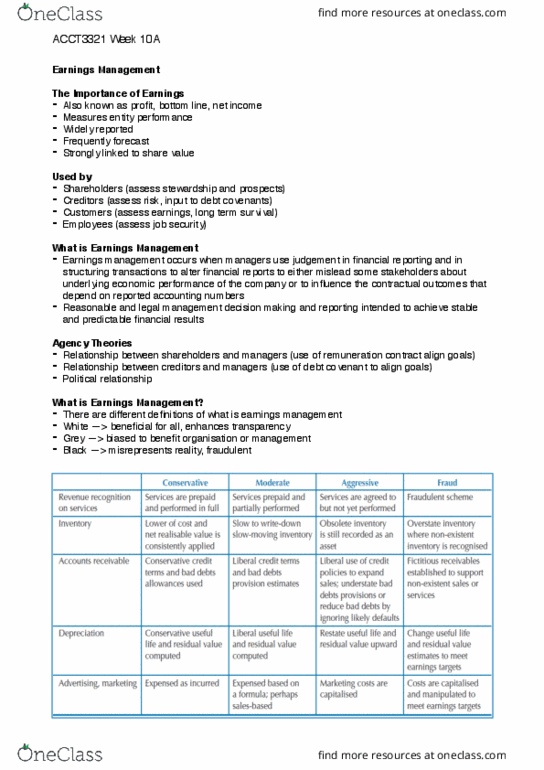

What is earnings management

find more resources at oneclass.com

find more resources at oneclass.com

- A purposeful intervention in the external financial reporting process with the intent

of obtaining some private gain

- Occurs when managers use judgement in financial reporting and in structuring

transactions to alter financial reports to either mislead some stakeholders about the

underlying economic performance of the company, or to influence the contractual

outcomes depending on reported accounting numbers

Methods of Earnings Management

-Accounting policy choice

oAccounting choices are made within the framework of applicable accounting

standards

oE.g. straight-line or reducing balance method, FIFO or weighted average…

oThese will lead to different timing amounts of expense recognition and asset

valuation

oEntities may change accounting methods in some circumstances

oProvided the entity can put a case forward to the auditors that the new

principle or practise is preferable, it is free to change this policy

oA change in accounting method could relate to a change in accounting

principle (e.g. depreciation method) or a change in accounting estimate (e.g.

useful life)

-Accrual accounting

oRather than reporting erratic changes in revenue and earnings year on year,

managers prefer to generate consistent revenues and earnings growth

oShareholders prefer to invest in an entity that exhibits consistent growth

patterns, not one that has uncertain and changing earnings patterns

oTherefore, managers use accrual accounting

oThey generally have no direct cash flow consequences and can include bad

debt expenses….

-Income Smoothing

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Sometimes called the bottom line or net income. Indicates to users the extent to which an entity has engaged in activities that add value to it the theoretical value of an entity"s stock is the present value of its future earnings. Earnings are used by shareholders to assess manager"s performance and to assist in predicting future cash flows and assessing risk. Lenders use earnings as a component in debt covenants to reduce the risk associated with lending and to monitor performance against covenants. A purposeful intervention in the external financial reporting process with the intent of obtaining some private gain. Income smoothing: smoothing moderates year-to-year fluctuations in income by shifting earnings from peak years to less successful periods, can relate to accrual accounting. Such as early recognition of sales revenue, variations to bad debts or warranty provisions, or delaying asset impairment.