BUSS1030 Lecture Notes - Lecture 4: Trial Balance, Current Asset, General Journal

24 Jul 2018

School

Department

Course

Professor

Document Summary

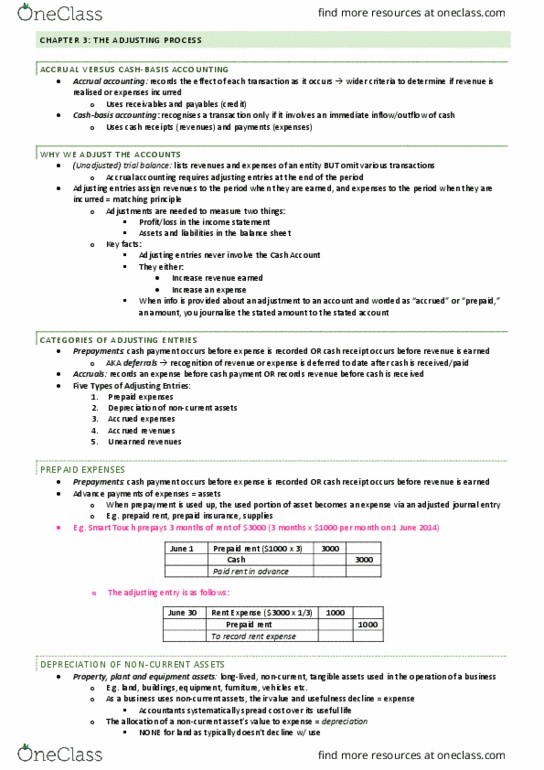

It doesn"t matter if you recognise something as an asset or expense first but adjusting entries is important eg. example: Bought of supplies but use of it by 31st jan: record asset. Calculating depreciation = (cost residual) / useful life: only for non-current assets eg. machine, equipment, except for land only non current asset not depreciated. Depreciation expense: dr depreciation expense, book value how much benefit remains of the asset (not the cost of what"s left, adjusting entry if you don"t do this then your profit is incorrect. If you don"t do this then your profit is overstated. If you don"t do this then your revenue is understated. Eg. you pay sydney morning herald for a 12 month supscription on the 1st of jan. Sydney morning herald cant write this down as revenue because they haven"t provided the service yet. Income statement / profit and loss statement / statement of financial performance is about revenue and expense.