FIN111 Lecture Notes - Lecture 9: Mortgage Insurance, Tertiary Education Fees In Australia, Credit Analysis

• Future and present values of multiple cash flows

• Valuing level cash flows: annuities and perpetuities

• Comparing rates: the effect of compounding periods

• Loan amortisation (ordinary annuity)

What is consumer credit?

• Power to buy or borrow on trust.

• Consumer credit is used to meet personal needs.

• Credit increases purchasing power in the short term.

Advantages of using credit:

Credit allows borrowers to

• Increase current purchasing power

• Transact efficiently

• Indicates good financial standing with external parties

• Reduces costs of holding cash

• Reduces record keeping

Disadvantages of using credit:

• Likelihood of overspending

• Reduction in quality of lifestyle if misused

• Adverse legal outcomes (court action, bankruptcy)

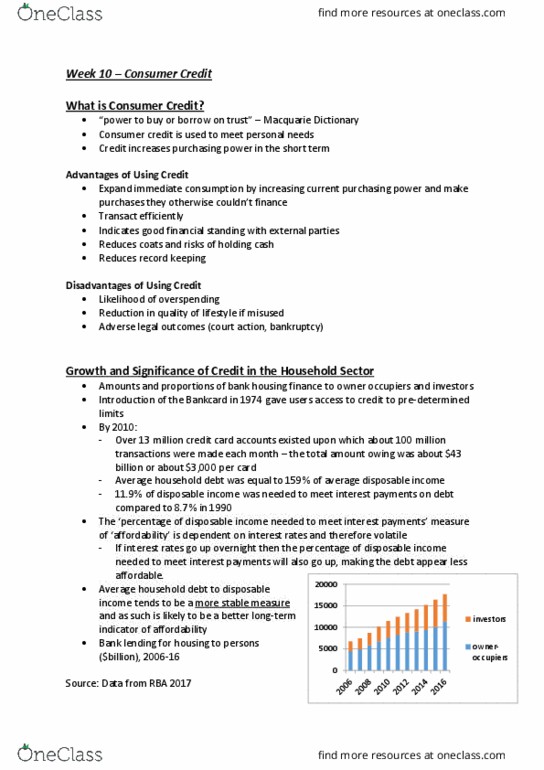

Growth of credit in the household sector:

• Amounts and proportions of bank housing finance to owner occupiers and investors.

• Bank lending for housing to persons (billions)

• Growth in bank finance for non-housing lending to individuals.

• Bank non-housing lending to persons (billions)

find more resources at oneclass.com

find more resources at oneclass.com

By 2010:

• Over 13 million credit card accounts existed upon which 100millions transactions were made

each month - the total amount owing was about $43 billion or about $3000 per card.

• Average household debt was equal to 159% of average disposable income.

• 11.9% of disposable income was needed to meet interest payments on debt compared to 8.7% in

1990.

• The amount of disposable interest payments needed to meet interest payments on disposable

debt since 1999-2013.

Whose debt?

• Proportion of debt by age range:

• Incidence of debt increases with income however debt stress is greater in lower-income

households.

Two basic types of consumer credit:

• Closed-End Credit:

• One time loans for a specific purpose that you pay back in a specified period of time, and in

payments of equal amounts.

• Mortgage, automobile, and instalment loans for furniture, appliances and electronics.

• Open-End Credit:

• Use as needed until line of credit max reached.

• E.g. credit cards, department store cards, home equity loans.

• You pay interest and finance charges if you do not pay the bill in full when due.

Types of credit:

1. Housing Loans

• 70% of Australian households live in a dwelling they either own or are buying.

• Owner-occupied housing loans are usually calculated on principal-and-reducing interest basis.

• Loan period typically varies between 15 to 30 years.

• Flexibility of housing loans provided by low-start/high start loans and fixed/variable interest

rates.

• Mortgage insurance required when loan-to-valuation ratios exceed 80-85%.

• Secondary mortgages market provides greater capital pool available for housing finance.

find more resources at oneclass.com

find more resources at oneclass.com