ACFI2070 Lecture Notes - Lecture 5: Liquid Oxygen, Tax Deduction, Tax Shield

29 Jun 2018

School

Department

Course

Professor

Module 2: Project Evaluation

Part 2.

Part one covered the basic valuation methods. This part concerns projects with different

lives, and alternative investment decisions. This part ultimately gives understanding of the

application of the NPV method, and gives techniques to compare mutually exclusive

projects with different lives via:

The lowest common multiple method

Constant chain of replacement in perpetuity

Equivalent annual value method

Learning Objectives:

1: Understand the principles used in estimating project cash flows.

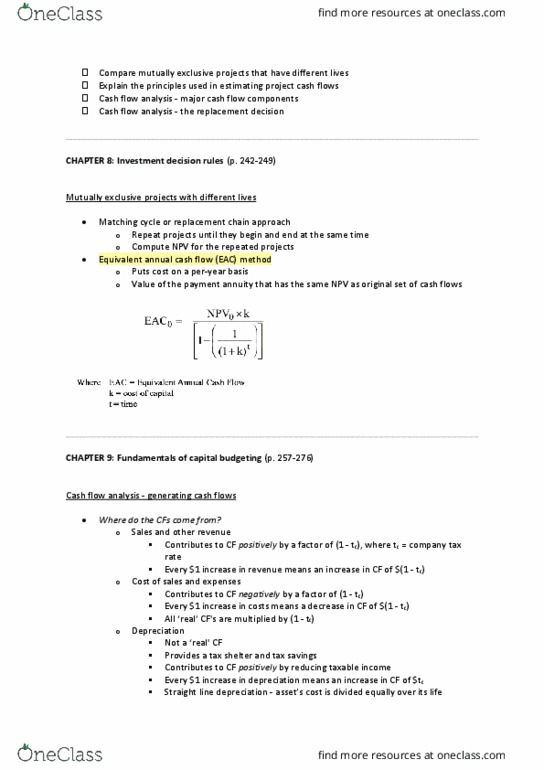

2: Compare mutually exclusive projects that have different lives.

3: Determine when to retire (abandon) or replace assets.

LO1: Application of the NPV Method

NPV is equal to the initial cash outflow + present values of future cash flows. What needs to be

determined is:

1. What are these cash flows?

2. Where do we get them?

3. What is the appropriate discount rate?

Suppose we want to open a Starbucks at Newspace in 2017. Suppose we could come up with reliable

estimates of our future sales and costs of the business, based on the number of workers and

students around and based on what other coffee shops are doing.

How do we estimate the actual $ we get from investing in this?

One way to answer this question is to estimate cash flows generated from this project, and

using the NPV method, see how much it is worth after deducting investment costs.

Free cash flow analysis: separation of investment and financing activities.

Free cash flow = cash flows that can be distributed to all financiers- we exclude debt payments from

FCF calculations. We do this as:

We don’t want to contaminate estimation of profitability of investment with how well we

finance it.

oSo to begin with, we assume we are financing investment with cash.

oOnce we understand the profitability of the project, we can then evaluate our

financing options.

find more resources at oneclass.com

find more resources at oneclass.com

oProject evaluation is a 2 step process (investment + financing).

To estimate the FCF:

Estimation of cash flows in project evaluation:

Recognise timing of cash flows:

oIs it a cash item?

oJust as in valuation of debt securities such as bonds, the exact timing of cash flows

can affect valuation of investment project.

oA simplifying assumption is that net cash flows are received at the end of a period.

Focus on incremental cash flows:

oWill the amount change if project is undertaken?

oOpportunity costs need to be accounted for.

Exclude sunk costs:

oSunk costs: cost that have already been incurred.

oWhether to continue project should be based only on expected future costs and

benefits.

Exclude financing charges:

oAvoid double counting financing charges in cash flows. The required rate of return

used to discount cash flows already incorporates both the costs of equity and debt.

Exclude allocated costs:

oAllocated costs: costs that are routinely allocated down or across an organisation

(for example, head-office expenses).

oAny costs which would be incurred and paid regardless of a potential new project’s

acceptance should be excluded from analysis.

Include residual values (if any).

oThis will provide cash flow at end of period.

Understand treatment of working capital:

oFor example, inventories, account payables/ recievables, etc.

oIncremental changes in the balance of working capital, and recovery of the full

balance of working capital are relevant cash flows.

Ensure consistency in the treatment of inflation:

oEstimate cash flows based on anticipated general price changes, and discount cash

flows using nominal rate, or

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

This part concerns projects with different lives, and alternative investment decisions. This part ultimately gives understanding of the application of the npv method, and gives techniques to compare mutually exclusive projects with different lives via: 1: understand the principles used in estimating project cash flows. 2: compare mutually exclusive projects that have different lives. 3: determine when to retire (abandon) or replace assets. Npv is equal to the initial cash outflow + present values of future cash flows. Suppose we want to open a starbucks at newspace in 2017. Suppose we could come up with reliable estimates of our future sales and costs of the business, based on the number of workers and students around and based on what other coffee shops are doing. One way to answer this question is to estimate cash flows generated from this project, and using the npv method, see how much it is worth after deducting investment costs.