ACCT2102 Lecture Notes - Lecture 10: Cost Driver, Deutsche Luft Hansa

ACCT2102: Variances

Variance Analysis: Variances can help to identify deviations from planned performance and be used for

evaluating performance and to motivate managers. Variances can help managers with their planning and

control functions as well with their strategy settings. For example, sometimes large variances can suggest

that the company should consider a change in strategy or a change in standard setting and control.

Variances effect on operating income: All variances can have either a favorable or an unfavorable impact

on operating incomes. Favorable variances have a positive impact on operating income and increase it

(relative to the budgeted amount), while unfavorable variances have a negative impact on the operating

income and decrease it.

Possible causes of a favorable direct materials price variance are:

- purchasing officer negotiated more skillfully than was planned in the budget,

- purchasing manager bought in larger lot sizes than budgeted, thus obtaining quantity

discounts,

- materials prices decreased unexpectedly due to, say, industry oversupply,

- budgeted purchase prices were set without careful analysis of the market, and

- purchasing manager received unfavorable terms on nonpurchase price factors (such as lower

quality materials).

Possible causes of an unfavorable direct manufacturing labor effciency variance

Some possible reasons for an unfavorable direct manufacturing labor efficiency variance are the hiring and

use of underskilled workers; inefficient scheduling of work so that the workforce was not optimally

occupied; poor maintenance of machines resulting in a high proportion of non-value- added labor; unrealistic

time standards. Each of these factors would result in actual direct manufacturing labor-hours being higher

than indicated by the standard work rate.

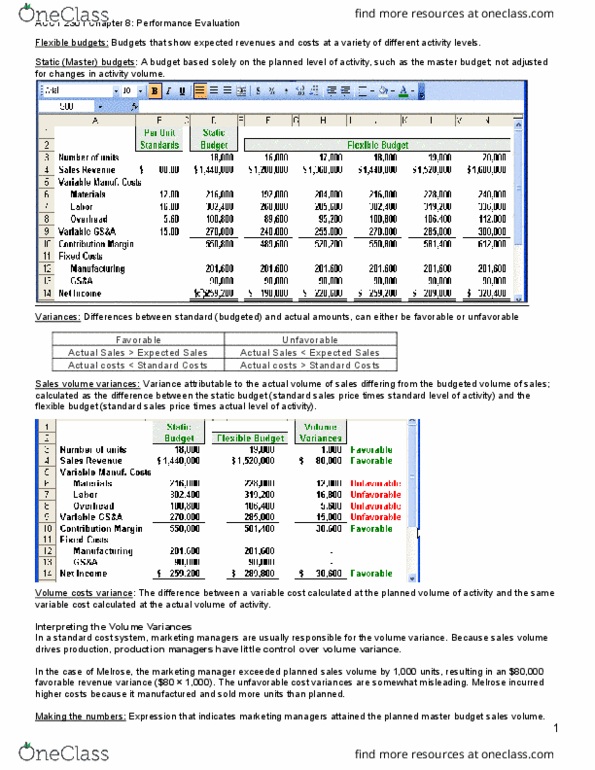

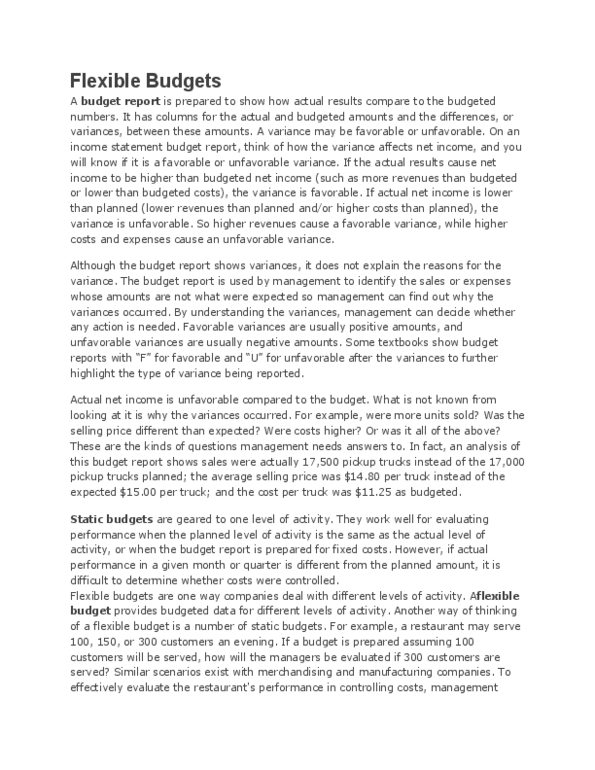

Variance analysis should be based on flexible budget instead of static budget.

Static budget ignores actual levels of output. It compares the budgeted costs/revenues for a planned level of

output versus actual costs/revenues for an actual level of output. The actual level of output may differ from

the planned level, and may necessitate different levels of costs.

Thus, the results could be misleading. For example, a favorable cost variance based on a flexible budget can

be changed to an unfavorable cost variance based on a static budget and, therefore, lead to wrong decision/s.

This is why performance of variance analyses should be based on flexible budgets.

Flexible budget vs Static budget

A flexible budget can be similar to a static budget if the actual outputs are equal to the planned outputs. This

is because the only difference between a static budget and a flexible budget is that the static budget is

prepared for the planned output, whereas the flexible budget is based on the actual output.

Standard costs:

Standard costs take into consideration issues related to the past costs such as past inefficiencies and take into

account expected future changes.

VARIANCES

Causes and responsibilities of different variances. Should they be investigated?

Materials Price Variance (MPV)

Purchase of materials

Responsibility: Purchasing manager. To get the best prices available for purchased goods and services

through skilful purchasing practices.

Causes: Higher price used for high-quality material?

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Variance analysis: variances can help to identify deviations from planned performance and be used for evaluating performance and to motivate managers. Variances can help managers with their planning and control functions as well with their strategy settings. For example, sometimes large variances can suggest that the company should consider a change in strategy or a change in standard setting and control. Variances effect on operating income: all variances can have either a favorable or an unfavorable impact on operating incomes. Favorable variances have a positive impact on operating income and increase it (relative to the budgeted amount), while unfavorable variances have a negative impact on the operating income and decrease it. Possible causes of a favorable direct materials price variance are: Purchasing of cer negotiated more skillfully than was planned in the budget, Purchasing manager bought in larger lot sizes than budgeted, thus obtaining quantity discounts, Materials prices decreased unexpectedly due to, say, industry oversupply,