ACCT1101 Lecture 10: L10

lOMoARcPSD|2476239

Lecture10:SustainableBusiness

‐

CorporateSocialResponsibility:managementphilosophythatincorporatesthebroaderpublic

interestintobusinessplanninganddecision‐making.Importanttofirmsbecauseenvironmentaland

socialimpactsareoftenbusinesscosts(emissiontaxes).

‐

AccountinginformationusedtoreportomCSRactivitiesandperformanceviafinancialstatements

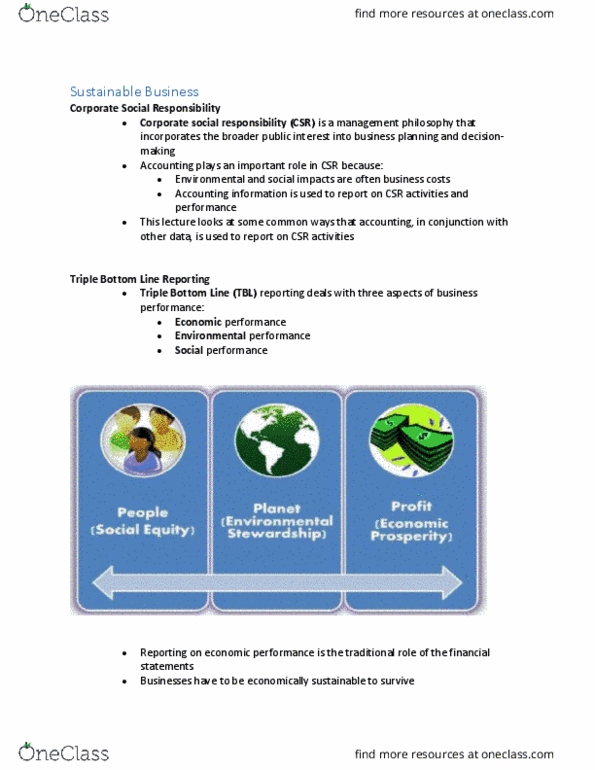

TripleBottomLine:considerseconomic(firmstatementsandwiderimpactslikejobscreated),

environmental,andsocialperformance.

‐

Environmentalperformance:usesindicatorslikeenergyuse,emissions,waste

‐

Socialperformance:howthebusinessinteractswiththecommunity.Indicatorslikeemployeerights,

education

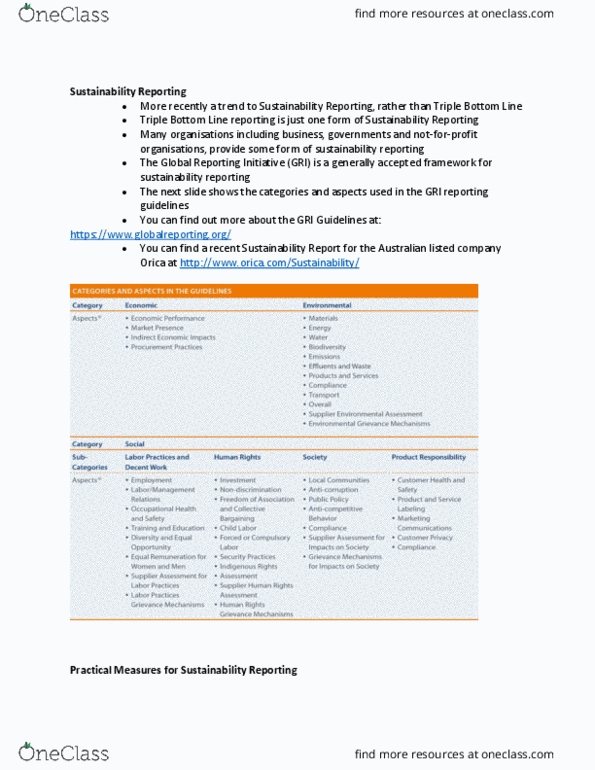

SustainabilityReporting:

‐

Increasingtrendforbusinesses,governmentsandnot‐for‐profitorganisationstoreporton

sustainabilityreporting

‐

Triplebottomlineisoneexampleofsustainabilityreporting

‐

GlobalReportingInitiativeisthegenerallyacceptedframeworkforsustainabilityreporting

‐

Sustainabilityreportingcontainsthreetechniques:lifecycleanalysis,materialcostflowaccounting,

eco‐efficiency

‐

Sharepercentagereferstoaproportionaloutputofanactivityvsitsoveralloutput(recycledwaste

asapercentageoftotalwaste).Alsoappliestopercentageofmaterialsinaproduct.

Lifecycleanalysis:usedtoassessthepotentialandrealenvironmentalimpactsduringallstagesofa

productslife.Usefultocompareproducts

‐

5stagestoaproductlifecycle;rawmaterialextractionandprocessing,productdesignand

manufacturing,packaginganddistribution,productuse,productendoflife

‐

Purposeistodesign,marketandmakemoresustainableproducts

‐

Lifecycleanalysisinvolves3stages;inventoryofpossiblematerialsandenergyrequiredfora

product,assessmentofactualandpotentialenvironmentalimpacts,reviewoftheproductto

asses/improvesustainability

‐

Hardtogatherandcollectalltherequiredinformationtodoanalysis

Materialcostflowaccounting:traceinputmaterialsthatflowthroughproductionprocessesandmeasure

theoutputofthoseproductionprocessesintermsoffinishedproductsandwaste

‐

Oftenformsapartoflifecycleanalysis

‐

Identifiescostsofwasteandemissions

‐

Workstoreducewasteandimproveproductivity(intheproductionprocess)

Eco‐efficiency:managementphilosophythatencouragesbusinesstosearchforenvironmental

improvementsthatyieldparalleleconomicbenefits.

‐

Determiningeco‐efficiencyofproductsandservicesisimportantpartinlifecycleanalysis

‐

Helpsto‘evaluatealternatives’howeverotherindicatorssuchasreliabilityandmaintenancecosts

alsoimportant

‐

Manyratiosareusedinmicroandmacroeconomicstocompareproductsbasedonecological

impactvscostacrossalternatives

‐

Comparativedatacanbehardtofindhowever

‐

Ecoefficiency=(product/servicevalue)/(environmentalinfluence)

EnvironmentalProjectAppraisal: