ACCT2112 Lecture Notes - Lecture 6: Underwriting, Income Statement, Capital Market

Document Summary

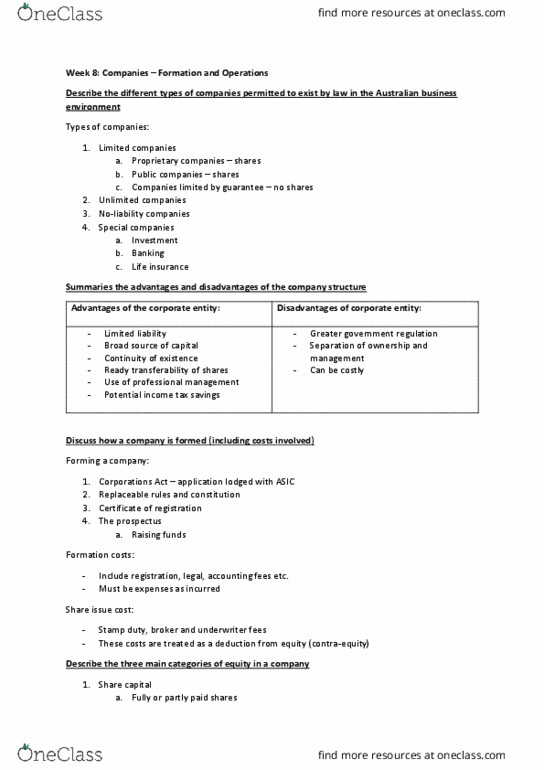

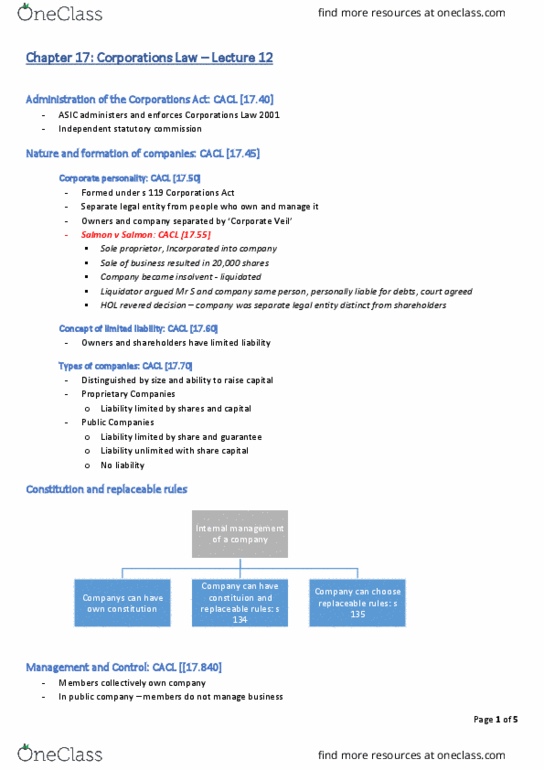

Advantages of corporate entity: limited liability, broad source of capital, continuity of existence, ready transferability of shares, use of professional management, potential income tax savings. Disadvantages of corporate entity: greater government regulation, separation of ownership and management. Forming a company: certificate of registration, replaceable rules/constitution, the prospectus. Categories of equity in company: income statement and asset/liability sections of balance sheet are the same for all forms of business organisation, equity of typical company split into 3 major categories, share capital, retained earnings, other reserves. Share capital: an equity account representing amount of assets invested by shareholders, ordinary shares/preference shares. Retained earnings: special reserve account reflecting amount of after-tax profits earned and retained in business, a debit balance is called accumulated loss . Other reserves: equity created as a result of application of gapp/accounting standards. Accounting for share issues: types of shares, ordinary shares, preference shares.