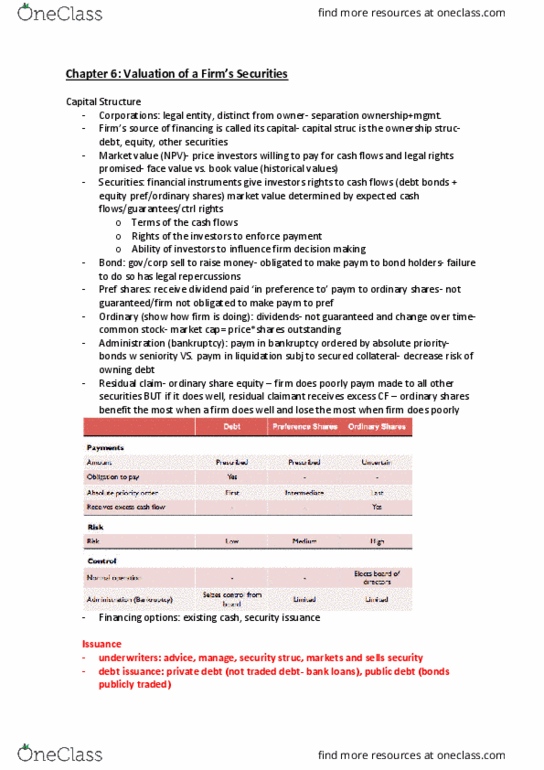

FINS1613 Lecture Notes - Lecture 11: Cash Flow, Tax Shield, Capital Structure

Document Summary

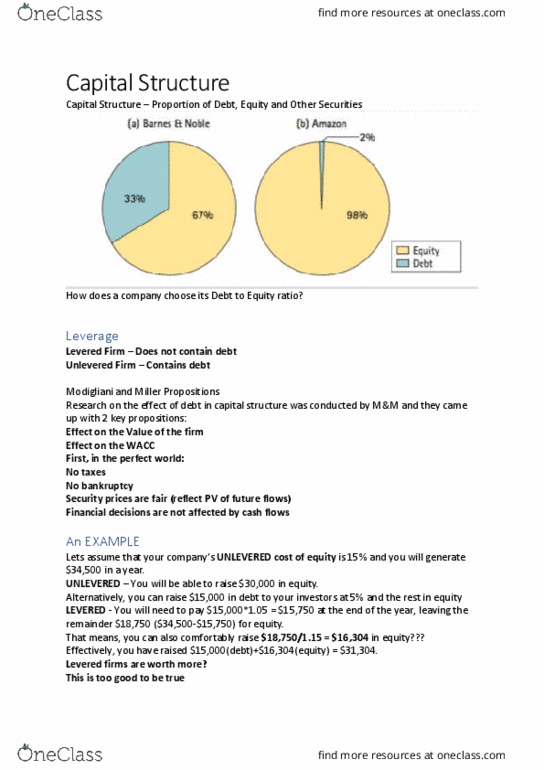

Capital markets have many frictions: taxes create a cash flow benefit for firms that have debt outstanding, administration is costly for the firm. The firm must decide which combination of debt and equity maximises the value of either a project or the overall firm: Value = pv(cash flows) + pv(interest tax shield) pv(financial distress costs) pv(issuance. Perfect capital markets have no frictions: taxes do not exist, administration is not costly for the firm. An unlevered firm is one that does not have any debt outstanding. A firm with debt outstanding is considered levered. In pcms, the wacc does not depend on the capital structure: Mm proposition i: in a perfect capital market, the total value of a firm is equal to the market value of the free flow cash flows generated by its assets and is not affected by capital structure: Interest tax shield: the reduction in taxes or gain to investors due to tax deductibility of interest payments: