FINS1613 Lecture Notes - Lecture 3: Preferred Stock, Capital Structure, Government Debt

Document Summary

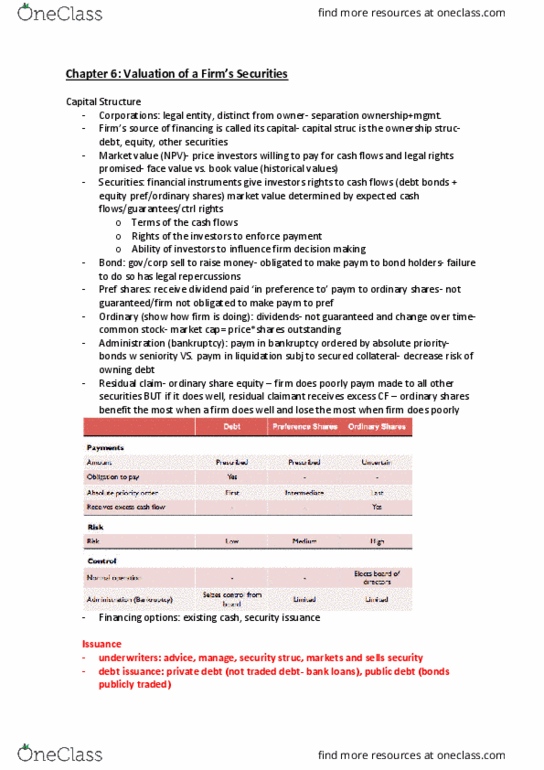

The fi(cid:396)(cid:373)"s sou(cid:396)(cid:272)e of fi(cid:374)a(cid:374)(cid:272)i(cid:374)g is (cid:272)alled its (cid:272)apital. The (cid:272)apital st(cid:396)u(cid:272)tu(cid:396)e is the o(cid:449)(cid:374)e(cid:396)ship structure of the firm and refers to the way a firm finances its overall operations and growth by using different sources of funds, i. e. the relative proportion of debt, equity and securities. Securities are financial instruments that give investors rights to cash flows for a firm. They are paid in preference from bonds then preference shares then ordinary shares. A bond collateralised by a manufacturing plant receives preference for cash received when the plant is sold: absolute priority and collateral decrease the risk of owning debt. O(cid:396)di(cid:374)a(cid:396)y sha(cid:396)e e(cid:395)uity is the (cid:396)esidual (cid:272)lai(cid:373) i(cid:374) a fi(cid:396)(cid:373)"s (cid:272)apital st(cid:396)u(cid:272)tu(cid:396)e, (cid:396)e(cid:272)ei(cid:448)i(cid:374)g (cid:272)ash flo(cid:449)s only after payments are made to all other securities. If a firm does poorly, payments to the residual claimant are stopped. However, when a firm does well, the residual claimant receives all the excess cash flows.