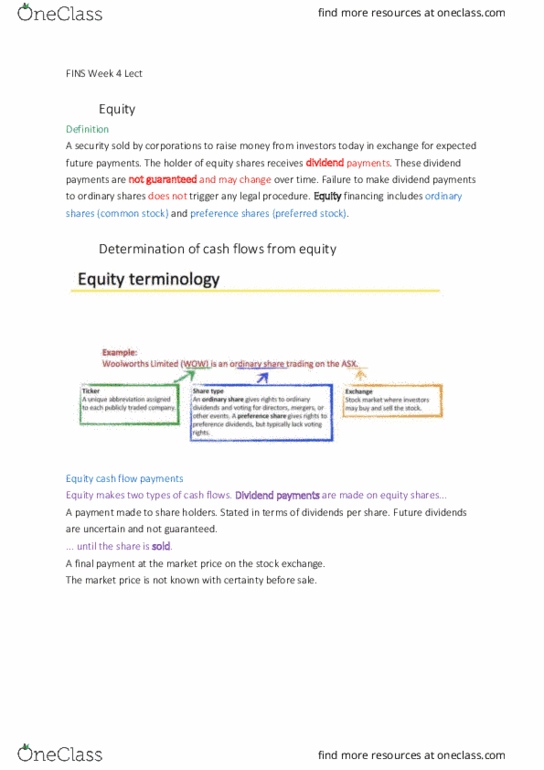

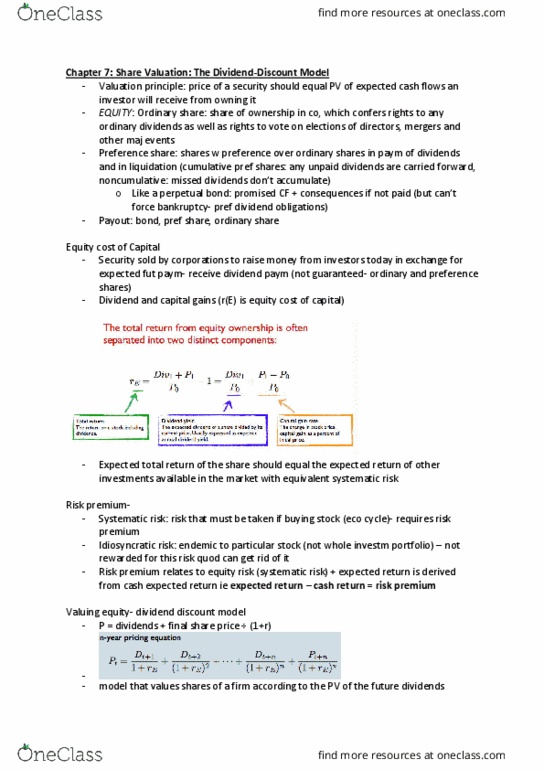

Calculating the market risk premium beta and required rate of return. CAPM. Portfolio Risk & Return.

We have a portfolio of three positively correlated but not perfectly correlated stocks.

(Correlation co-efficient between 0-1)

Stock Expected Rate of Return Standard Deviation Beta

X 10% 16% .75

Y 12% 16% 1.25

Z 13% 16% 1.50

What is the market risk premium for the portfolio ?

Required Rate of Return For the Stock = Risk Free rate of Return +

+ ( Market Risk Premium * Beta of stock )

Market Risk Premium = Market Required Rate of Return â Risk Free rate of Return

The returns on stocks X, Y and Z and their beta have been provided. Using the information provided, we will first calculate the market risk premium.

The capital asset pricing model is a model based on the proposition that any stock's required rate of return is equal to the risk free rate of return plus a risk premium that reflects only the risk remaining after diversification.

The required rate of return for a stock is calculated by adding the risk free rate of return to the product of the market risk premium and the stock's beta.

The market risk premium shows the premium that investors require for bearing the risk of average stock and is calculated by deducting the risk free rate from the market's required rate of return.

Now, using stock X or any other stock, we can calculate the market risk premium. We'll use stock X. The expected return on this stock is 10%. The risk free rate is 7& and the stock's beta is .75.

By solving the equation we determine the market risk premium to be 4%.

Next, we will calculate the beta of Fund Q.

Fund Q has 1/3 of its funds invested in each of the three stocks X, Y, and Z.

Thus, the beta of Fund Q will be the sum of one third of the beta of each stock. One third of .75 is .25. One third of 1.25 is .4167 and one third of 1.5 is .5. By adding .25, .4167 and .5, we calculate the beta of Fund Q as 1.1667.

Letâs now calculate the required return of Fund Q. The risk free rate is 7%. The market risk premium is calculated to be 4%. The beta of Fund Q is 1.1667. By adding 7% to the product of 4% and 1.1667, we determine the required return on Fund Q to be 11.67%.

Since the returns on the three stocks included in Fund Q are not positively correlated, the standard deviation of the fund will be less than 16%.