FINS1612 Lecture Notes - Lecture 7: Overdraft, Matching Principle, Byrsonima Crassifolia

Monday, 24 April 2017

Capital Markets & Institution

Debt Markets

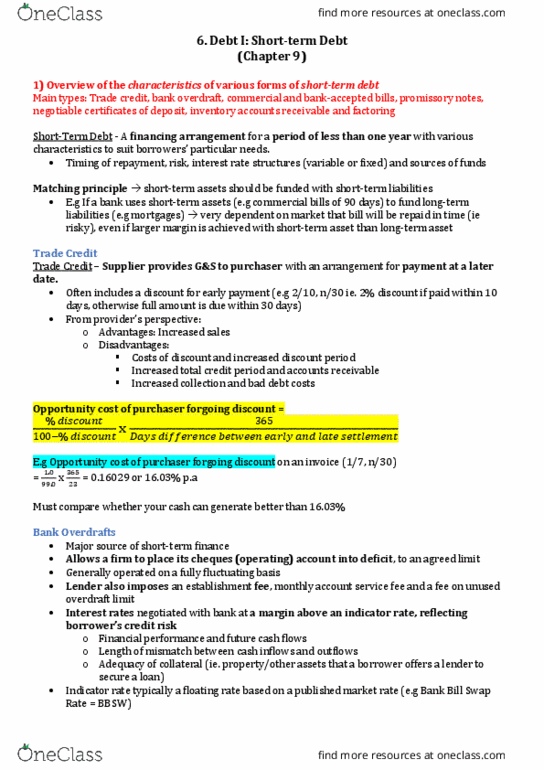

-Short-Term Debt: A debt financing arrangement for a period of less than one year

•Sub-prime loans - where a lender waives normal lending criteria in order to provide

a loan to a party who otherwise could not obtain a loan

-Catalyst for GFC (matching principle not adhered to) - short-term debt dried up &

banks unable to fund longer term loans they had advanced

-Trade Credit: Supplier provides goods to a purchaser with an arrangement for

payment at a later date

•Pay early to get a discount, otherwise pay full amount

•Accounts receivable - records amounts owing to business (ie trade credit)

•Relaxation of trade credit standards may attract customers, but also increases

likelihood of bad debts

-Overdraft Facility: Fluctuating credit facility provided by bank; allows a business

operating account to go into debit up to an agreed limit

•Operating account - cheque account through which firm conducts day-to-day

financial transactions

•Interest rate payable on overdraft is negotiated between bank & firm

-Normally at margin above periodically published reference interest rate (used for

pricing variable-rate loans)

•Banks require an overdraft to be operated on a fully fluctuating basis

-Borrower expected to bring overdraft back into credit from time to time

•Establishment fee - charged by bank to cover costs associated with evaluating a

loan application (overdraft)

•Banks asses adequacy of collateral (or security) available if borrower defaults

-Property or other assets pledged to lender as security to support a loan

-Bill of Exchange: Short-term money-market discount security; face value repayable at

maturity

•Commercial Bills:

-Maturities range up to 180 days

!1

find more resources at oneclass.com

find more resources at oneclass.com

Monday, 24 April 2017

-Does not pay interest

-Drawer is issuer of bill

-Acceptor is bank who gives bill more credit (primary liability to repay bill)

-Payee receives funds when bill is initially discounted (usually drawer)

-Discounter is buyer of the bill (investor)

-Endorser signs bill on reverse when sold (legal chain of ownership)

•Establishing a Bill Financing Facility:

-Rollover facility - arrangement whereby bank agrees to discount new securities

over a specified period as the existing securities mature

-Bill line - arrangement whereby a bank agrees to progressively discount bills up to

an agreed amount

-Promissory Notes: Discount securities issued by corporations without an acceptor or

endorsement (aka commercial paper)

•Face value payable at maturity - range up to 180 days (6 months)

•No acceptor - only corporations with high credit rating able to issue

•Roll-over - after maturity, new notes issued & discounted (e.g. another 6 months)

•Sole liability to repay P-note at maturity lies with issuer

•Face value normally minimum of $100 000 (some in excess of $1bn)

•Lead manager - arranger of a syndicated debt facility; structures issue, forms

syndicate & prepares documentation

•Dealer panel - panel members promote & distribute debt issues to clients & maintain

a secondary market in the paper

•Tender - dealers bid competitively for paper

•Tap issuance - issues made progressively, subject to investor demand

•Dealer bids - members of dealer panel asked to bid for paper

•Underwritten P-notes:

-P-notes may be unsuccessful without string name or reputation of business, issue

is incorrectly priced, credit rating is below investment grade

-Underwriting syndicate - promoters of an issue who agree to purchase paper not

taken up by tender panel

-Involves fee & rollover facility usually established (extended line of credit)

•Issuing programs:

-Usually arranged by major commercial banks & money market corporations

!2

find more resources at oneclass.com

find more resources at oneclass.com

Monday, 24 April 2017

-Standardised documentation

-Revolving facility

-Most P-notes issued for 90 days

-Negotiable Certificates of Deposit (CD): Discount security issued by a bank

•Typical initial term maturity up to 180 days

•Banks may use CDs to manage their:

-Liability needs

-Liquidity needs (daily cash flows)

•Active secondary market in CDs

-Inventory Finance: Provided to retail outlet to fund purchase of stock

•‘Floor plan finance’ - provision of finance for stock on a showroom floor (e.g. motor

vehicle dealer)

-Bailment is common - finance company holds title to dealership’s stock

-Bailor is finance company & bailee is vehicle dealership

-Accounts Receivable Financing: Company uses its accounts receivable debtors as

security to support loans

•Mainly supplied by finance companies (some banks)

•Lending company takes charge of company’s accounts receivable (borrowing

company still responsible for debtor book & bad debts)

-Factoring: Company sells accounts receivable at discount to a factor company to

generate immediate cash flows (raise funds)

•Factor company responsible for collection of accounts receivables

•Notification basis - vendor required to notify its (accounts receivables) customers

that payment is to be made to the factor

•Non-notification basis - accounts receivables paid by firm’s debtors directly to an

address controlled by factor (not actually to factor)

•With-recourse factoring - factor has claim against vendor if a receivable is not paid

•Non-recourse factoring - factor has no claim against vendor company

!3

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Catalyst for gfc (matching principle not adhered to) - short-term debt dried up & banks unable to fund longer term loans they had advanced. Overdraft facility: fluctuating credit facility provided by bank; allows a business operating account to go into debit up to an agreed limit: operating account - cheque account through which rm conducts day-to-day. Nancial transactions: interest rate payable on overdraft is negotiated between bank & rm. Normally at margin above periodically published reference interest rate (used for pricing variable-rate loans: banks require an overdraft to be operated on a fully uctuating basis. Property or other assets pledged to lender as security to support a loan. Bill of exchange: short-term money-market discount security; face value repayable at maturity: commercial bills: Acceptor is bank who gives bill more credit (primary liability to repay bill) Payee receives funds when bill is initially discounted (usually drawer) Discounter is buyer of the bill (investor)