BSB110 Lecture Notes - Lecture 7: Internal Control, General Ledger, Accounts Payable

Accounting – Accounting Information Systems

Principles

- Cost benefit analysis

oIs it worth implementing an accounting information system?

- Useful output

oIs the information relevant

oIt is timely

oMay miss out on critical decision-making information if recording is not timely

- Comparable

oMultiple dimensions

oGeography considerations

- Flexibility

oCompatible with business life cycle

oTechnological advances, increased competition, changing accounting principles,

organisational growth, government regulation and de-regulation

Implementing an accounting system

- Run along with old system in case there are any problems

- Any tweaking required?

Developing an Accounting System

- Must have controls to ensure assets are safeguarded and relevant, timely, and faithfully

represented information is provided

- Risks of confidential and sensitive information being leaked are minimised

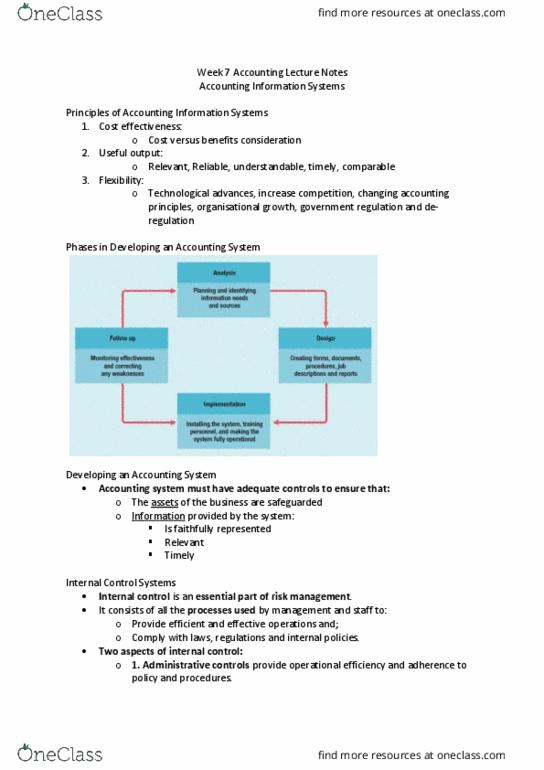

- Phases

oAnalysis – Planning and identifying information needs and sources

oDesign – Creating forms, documents, procedures, job descriptions and reports

oImplementation – Installing the system, training personnel, and making the system

fully operational

oFollow up – Monitoring effectiveness and correcting any weaknesses

Internal Control Systems

- Essential part of risk management

- Put in place in the organisation to minimise business risks

- Two aspects

oAdministrative

Provide operational efficiency and adherence to policy and procedures

Physical

Policies and Procedures

oAccounting

Methods and procedures used to protect assets and ensure that

transactions are recorded appropriately

How do businesses make sure they have accounting controls in place when

they process their transactions so they are reporting as accurately as

possible?

- Management Responsibility

oPart of good corporate governance for managers to be responsible for developing

appropriate controls

oManagers cannot abuse their power

oManagers should not be the owners

- Internal auditing

oIdentify if people are adhering to procedures

oMonitor effectiveness of internal controls

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Useful output: is the information relevant, it is timely, may miss out on critical decision-making information if recording is not timely. Flexibility: compatible with business life cycle, technological advances, increased competition, changing accounting principles, organisational growth, government regulation and de-regulation. Run along with old system in case there are any problems. Must have controls to ensure assets are safeguarded and relevant, timely, and faithfully represented information is provided. Risks of confidential and sensitive information being leaked are minimised. Put in place in the organisation to minimise business risks. Provide operational efficiency and adherence to policy and procedures. Methods and procedures used to protect assets and ensure that transactions are recorded appropriately. Management responsibility: part of good corporate governance for managers to be responsible for developing appropriate controls, managers cannot abuse their power, managers should not be the owners. Internal auditing: identify if people are adhering to procedures, monitor effectiveness of internal controls.