BSB110 Lecture Notes - Lecture 6: Gross Profit, Current Asset, Weighted Arithmetic Mean

Accounting – Inventories

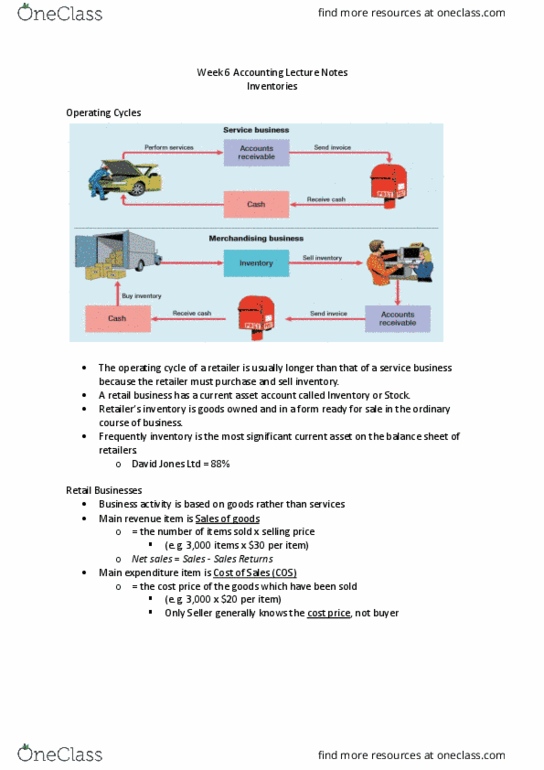

Operating cycles

- Longer for retail then service business

- Need time to buy stock and have it delivered and then sell it

- Inventory is the most significant current asset

Retail businesses

- Main revenue from sales of goods

- Main expenditure is cost of sales

- How is the cost determined?

- Inventory – goods held for resale e.g. clothes, food, petrol, electrical goods

Merchandising Operations

- Sales revenue – cost of sales = gross profit

- Gross profit – operating expenses = profit (loss)

Management of inventory

- Efficient handling of inventory

oAs minimal as possible

oToo little may lead to loss

oToo much is expensive and ties up cash

- Safeguarding stock

oHow do businesses make sure customers are paying the right amount for the right

product?

oSelf-checkout

oStocktake

- Fire-sale of inventory

oSell quickly and under normal cost

oDone when businesses are in danger of bankruptcy

oPoor management can lead to losses and eventual collapse e.g. Dick Smith

Inventory Systems

- Two types

- Periodic

oDetailed records are not maintained

oNot a running record

oCost of sales is determined at the only of the accounting period by a physical

inventory account

oUpdated periodically e.g. once a month (depends of the size of the business)

oUsed by small businesses e.g. sole proprietorships

- Perpetual

oKeeping continuous record of movement

oLarge companies e.g. supermarkets, department stores

oBar codes and optical scanners

Recording purchases of inventories in a periodic inventory system

- Purchases account used to record cost of all inventory purchased

- When buying things from suppliers

oExpense – Dr account

oJournal entry

Dr to expense

Cr to liability

om/n – If you pay within n amount of days, you get m% off (e.g. 2/7 – pay within 7

days, get 2% off)

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Need time to buy stock and have it delivered and then sell it. Inventory goods held for resale e. g. clothes, food, petrol, electrical goods. Sales revenue cost of sales = gross profit. Gross profit operating expenses = profit (loss) Efficient handling of inventory: as minimal as possible, too little may lead to loss, too much is expensive and ties up cash. Safeguarding stock: how do businesses make sure customers are paying the right amount for the right product, self-checkout, stocktake. Fire-sale of inventory: sell quickly and under normal cost, done when businesses are in danger of bankruptcy, poor management can lead to losses and eventual collapse e. g. dick smith. Perpetual: keeping continuous record of movement, large companies e. g. supermarkets, department stores, bar codes and optical scanners. Recording purchases of inventories in a periodic inventory system. Purchases account used to record cost of all inventory purchased. When buying things from suppliers: expense dr account, journal entry.