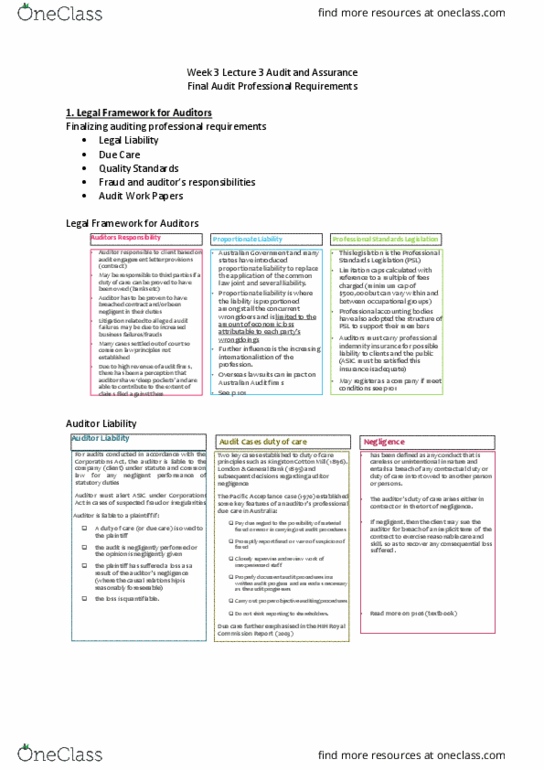

AYB301 Lecture Notes - Lecture 2: Fiduciary, Corporations Act 2001, Financial Statement

Document Summary

Professional ethics, independence: duties of professional auditor, five attributes of a profession, 1. A culture: professional characteristics, mastery of a particular intellectual skill, adherence to a common code of values and conduct, acceptance of a duty to society as a whole, duties of a profession: Integrity in client dealings: competence in the field of expertise and knowledge, objectivity in offering services, confidentiality in client matters, discipline over members who do not discharge these duties according to public expectations, see greenwood (1957) Integrity: exercise of due care, objectivity, confidentiality, competence. Independence (conflict of interest, gifts and hospitality: assumes a commitment to put the public, client. Ethical understanding: linking professionalism to ethics, ethics, a set of moral principles or values - usually different for each person: Details of the code part b: relevant sections of the code, complying with the code s100. Assessment 1: threats, 120. 6 a3 threats to compliance, a.