BTC3150 Lecture 3: Week 3

Week$3a:$Income$from$business$

$

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!Gains!from!

!

!

!

!

!

!

!

!

!

!

!

!

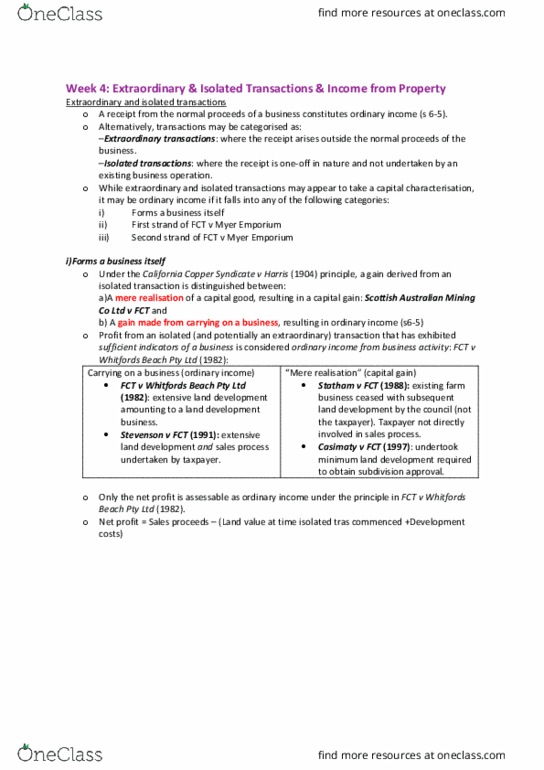

Receipts$from$business$activity$

Characteristics!of!receipts!as!ordinary!income!from!a!business!activity!involves!a!

Two!step!process:!

a) Determining!whether!the!taxpayer!is$carrying(on(a(business$

b) Consideration!of!whether!the$receipts(are(the(normal(proceeds(of(that(business(

activity(

!

a) Determining$whether$the$taxpayer$is$carrying$on$a$business$

• Hobby!vs!Business$

• Business!(s!995-1):$

- includes!any!profession,!trade,!employment,!vocation!or!calling,!but!does!not!

include!occupation!as!an!employee!!

!

!!!!!!!!!!!!!!Indicators$of$a$business$activity$by$courts:$

o Profit-making!intent:!

- Not!necessary!to!show!actual!profit!to!show!intent!

- Lack!of!profit-making!intention!doesn’t!necessarily!preclude!there!being!a!

business:!

- !CL:!Stone(v(FCT((2005):!Policewoman!javelin!thrower.!Had!skills!and!talent,!

generating!income!from!being!a!javelin!thrower-!constituted!to!carrying!on!a!

business!in!relation!to!her!sporting!act,!therefore!income!from!competitions!

are!ord!income!under!s6-5$ITAA97.!

o Scale!of!activities,!including!the!nature!and!type!of!capital!and!level!of!turnover:!

- Small!operation!can!still!constitute!a!business!if!there!are!sufficient!other!

characteristics:!!

- CL:!FCT(v(JR(Walker((1985).!Working!on!land,goats!–!profit!intention.!

!

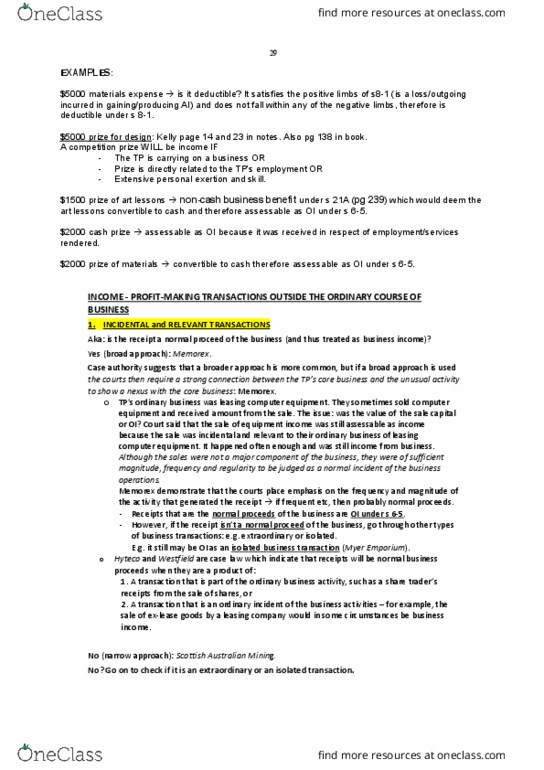

Carrying!on!business!

$$$$$$$$$$$$S6-5$

Non-business!activities!

(hobbies)!

Not!assessable!income,!unless:!

i) Another!general!concept!of!

ordinary!income!applied!

(extraordinary!transactions)!or!

ii) Specifically!made!assessable!by!

legislation!(statutory!income)!

Constitutes!ordinary!

income!

o Commercial!approach!is!taken:professional!advice!during!operations,!if!market!for!

produce!has!been!explored,needed!for!domestic!purposes!

!CL:!Thomas(v(FCT((1972):!

o System!and!organisation!employed:!

- Degree!of!planning!and!amount!of!time!invested!

- Taxpayer!may!delegate!these!duties!and!still!be!considered!a!business:!

- CL:!Ferguson(v(FCT((1979)!!-!retired!navy!whom!raised!cattle.!!

o !Methods!characteristic!of!the!particular!line!of!business!

- Dairy!farmer!use!planned!breeding!programs!

o Sustained!and!frequent!activity!

– Output!much!greater!than!what!needed!for!domestic!purposes:!!

– CL:!Thomas(v(FCT((1972)!–!did!not!make!profit,!made!losses!but!still!a!business!

although!main!income!was!from!being!a!barrister.Tree!planting!was!uch!greater!

than!needed!domestic!purposes-!more!than!just!a!hobby.!

o The!type!of!activity!and!the!type!of!taxpayer.!

!

Hobby$vs$Business$

1) Gambling!

o Professional!bookmakers!and!casino!operators!carry!on!a!gambling!business!(scale,!

commerciality,!profit-intention).!

o Individuals!who!gamble!are!very!unlikely!to!be!considered!a!business,!unless!a!

significant!degree!of!indicators!exist,!for!example:!

!

$$$$$$$$$$$$$Gambling$business!

Not$a$business!

!

•Trautwein*v*FCT*(1936):!horse!

racing!with!view!to!profit;!farm!to!

breed!horses;!racing!own!horses!

and!those!leased;!frequent!and!

systematic!betting;!wagering!

large!amount!of!money;!use!of!

agent!to!bet;!attended!race!

meetings.!

•Evans*v*FCT*(1989):!horse!

betting!over!five!year!period;!

“lucky!gambler”’;!bets!not!

placed!with!a!bookmaker;!

wagered!on!long-odds!bets.!

!

!

2) Sportspeople!

o Determine!whether!the!receipts!derived!by!a!professional!sportsperson!is!from!a!

business!or!personal!services:!

- An!employee!has!limited!deductions!compared!to!a!business.!

o Courts!have!tended!to!more!likely!label!professional!sportspeople!as!being!in!

business:!

- Olympian!(also!a!full-time!police!officer)!derived!among!other!things:!prize!

money,!sponsorship!and!appearance!fees.!No!clear!profit!motive:!Stone(v(FCT(

(2005).!

- Playing!football!full-time,!sports!managers!(representatives),!ancillary!

activities!such!as!endorsements!and!media!arrangements:!Spriggs(v(FCT;(

Riddell(v(FCT((2009).!

!

!

!

!

!

3) Investment!activities!

!

A!business!of!investment!can!exist!where!there!is!sufficient!indicators!of!a!business:!

!

Taxation!consequences:!

–If!a!business,!the!investment!(eg!shares)!will!be!treated!as!trading!stock!and!hence!on!

revenue!account.!

–If!not!a!business:!the!investment!is!on!capital!account.!

!

4) Land!sales!

!!!!! !

!

Note:!notwithstanding!a!prima(facie!capital!characterisation,!activities!of!land!development!

could!constitute!an!extraordinary!or!isolated!transaction.!

!

5) Sharing!economy!–!other!people!helping!each!other!

!!!!!!! !

•Difficult!to!argue!that!the!provider’s!actions!are!in!pursuit!of!a!recreational!activity,!for!

example:!Eg!UBER!

–Pricing!indicates!intention!to!profit!

–Operation!may!be!small!but!business-like!approach!

–Level!of!detail,!professionalism!and!organisation.!

Investment!business!

Not!a!business!

•London*Australia*Investment*Co*Ltd*vFCT:*

High!degree!of!investing!and!re-investing!in!

shares!to!maintain!a!high!degree!of!

dividend!yield.!

•AGC*(Investments)*Ltd*v*FCT*(1992):!!

Invests!for!the!long!term-growth,!rather!

than!speculative!investment.!

Capital:!selling!

land!one-off!

!

Income:!Property!

developers!

Document Summary

Another general concept of ordinary income applied (extraordinary transactions) or. Characteristics of receipts as ordinary income from a business activity involves a. Indicators of a business activity by courts: profit-making intent: Not necessary to show actual profit to show intent. Lack of profit-making intention doesn"t necessarily preclude there being a business: Cl: stone v fct (2005): policewoman javelin thrower. Small operation can still constitute a business if there are sufficient other characteristics: Working on land,goats profit intention: commercial approach is taken:professional advice during operations, if market for produce has been explored,needed for domestic purposes. Cl: thomas v fct (1972): system and organisation employed: Degree of planning and amount of time invested. Taxpayer may delegate these duties and still be considered a business: Cl: ferguson v fct (1979) - retired navy whom raised cattle. Methods characteristic of the particular line of business. Dairy farmer use planned breeding programs: sustained and frequent activity. Output much greater than what needed for domestic purposes: