BTC3150 Lecture Notes - Lecture 2: Qantas, Capital Asset, Labor Rights

Week$2a:$Residence$&$Source$

!

General!principles:!

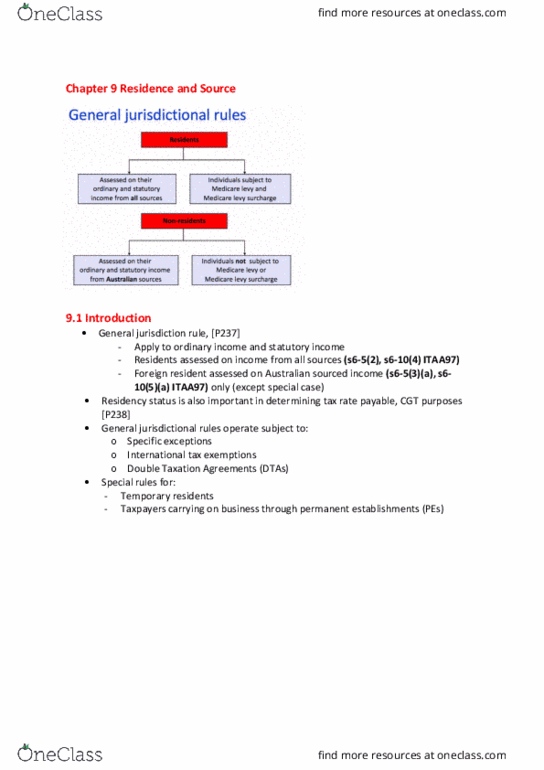

• A!resident$of$Australia!for!tax!purposes!will!be!taxed!on!income!from!all!sources:!

– See,!s$6-5(2)!ITAA97.!

• A$foreign$resident!for!tax!purposes!will!be!taxed!on!income!from!Australian!sources!

only:!

– See,!s$6-5(3)!ITAA97.!

!

Tax$residency:$impact$on$individual$taxpayers$

• Individual!tax!rates:!

§ Differ!depending!on!whether!the!individual!tax!payer!is!a!resident!for!tax!

purposes!or!a!foreign!resident.!

§ Broadly,!a!foreign!resident!does!not!receive!the!benefit!of!the!tax-free!

threshold.!

• Foreign!residents!:!

§ do!not!have!access!to!many!personal!tax!offsets.!

§ not!liable!for!the!Medicare!levy.!

To$determine$taxpayer’s$ordinary$income.$

When$is$a$taxpayer$a$tax$resident$of$Australia?$

!! !

$

A) Individuals$S6(1)$ITAA36$

Only!one!of!the!four!tests!needs!to!be!satisfied!to!be!tax!resident:!

!

!" #$%&'$%()$%)(*+$%&'$,-$(.--/+'&,0()/(/+'&,.+1(-/,-$2)%"(

• Determination!of!tax!residency!rests!on!a!question!of!fact!and!degree:!!"##$%&'&()*&

(1946).!

• Term!“resides”!is!not!defined!in!statute.!

!

!!!!!!!(+,-.%/&,.0/"1$%$1&23&-4$&,.5%-/&

• Time!physically!spent!in!Australia.!

• If!the!person!is!a!visitor,!the!frequency,!regularity!and!duration!of!visits:!!

)67&89)&'&63/+:4-&;<=>?@&A&7&.0$&B$$C&$+,4&D.0-4&"0&-4$&EFG&$/-+2#"/4$1&+&H#+,$&.I&

+2.1$&"0&8%$#+01G&4+1&2+0C&+,,.50-/&"0&2.-4&EF&J&8%$#+01K&7&L&%$/"1$0-&2+/$1&.0&

-4$&%$:5#+%"-3&.I&'"/"-"0:&EF&15$&-.&.2#":+-".0.!!

• Purpose!of!the!visits!to!Australia!and!abroad.!

• The!maintenance!of!a!place!of!abode(home)!in!Australia!for!the!taxpayer’s!use.!

• The!person’s!family,!business!and!social!ties:!!

CL:!6$'$0$&'&89)&[1928]!–!purpose!were!nothing!more!than!temporary!(eg!visit!

relatives,!obtain!medical!advice,!attend!religious!ceremonies)!

• The!person’s!nationality!may!be!considered!for!borderline!cases.(not!a!strong!

factor!though)!

!

&&&&&&&&&*4$&).DD"//".0$%&.I&*+M+-".0N/&'"$B&

• The!Commissioner!places!emphasis!on:!

–Intention!or!purpose!of!presence!

–Family!and!business!or!employment!ties!

–Maintenance!and!location!of!assets!

–Social!and!living!arrangements.!

• In!addition!to!the!above!behavioural!characteristics!of!the!taxpayer,!the!

Commissioner!considers!there!must!be!sufficient!time!elapsed!to!demonstrate!

continuity,!routine!or!habit!(physical!presence!in!Aus)!

Example:Ruling!TR!98/17!

A) Bjorn!18!month!Contract,!did!not!perform,!went!back.!Resident-intented!to!stay!

for!18mtnh!w!his!family,behaviour!consistent!wit!intention!

B) Michael!uni!–!Foreign!resident!as!he!did!not!exhibit!consistent!with!residing!to!

Aus-!returns!to!SA!after!8!onth!course.!

- 183!test!considered!–!stll!not!a!resident!as!his!usual!place!of!abde!is!outside!

of!Aus!&!does!not!intend!to!take!up!residence!in!Aus!

C) Michelle-!conduct!reasarch,!family!in!borsedaux,!had!to!go!back.!Foreign!

resident-quality!of!her!stay!&!charater!are!closer!to!a!visitor.!

!

3" 4/5&-&6$()$%)(*78$+$(1/9(+$%&'$:6&;$"<(%).)9)/+1()$%)(

• An!individual!is!a!resident!of!Australia!if!his!or!her!domicile!is!in!Australia,!unless!

the!Commissioner!is!satisfied!that!the!person!has!a!permanent!place!of!abode!

outside!Australia.!

• RuLE!OF!THUMB: 2 YEARS ITA 2650!

If!a!taxpayer!leaves!Australia!and!intends!to!return!within!2!years,!then!they!will!

not!have!a!permanent!place!of!abode!overseas.!(Still!consider!other!factors)!

• Domicile’!is!determined!according!to!the!O.D","#$&L,-&<=?>7!

–Domicile!of!origin!at!birth!

–Domicile!of!choice:!country!where!the!taxpayer!intends!to!make!their!home!

indefinitely.!

• Generally!applies!to!individuals!moving!overseas!(eg,!usually!as!a!work!posting),!!

!

&&&&&&&P$%D+0$0-&H#+,$&.I&+2.1$&.5-/"1$&L5/-%+#"+&

• The!domicile!test!does!not!apply!when!the!individual!can!demonstrate!that!he!or!

she!does!not!have!a!“permanent!place!of!abode!outside!Australia”.!

– CL:!=$'$+.6(>/55&%%&/,$+(/?(@.A.)&/,(;(B226$0.)$C(

–!Taxpayer!moved!to!Vila!and!stayed!there!for!two!years!but!returned!on!one!

occasion!when!his!wife!had!a!baby.!The!taxpayer!became!ill!iand!returned!to!

Australia.!

–High!Court!held!that!permanent!does!not!mean!“forever”-!not!ever!lasting!and!

is!assessed!objectively!each!year. the!taxpayer!had!abandoned!his!Australian!

home!and!intended!to!stay!in!Vanuatu!for!an!indefinite!period.!Had!a!place!of!

abode!outside!Aus!–!non-resident.!

– CL:!FCT!v!Jenkins!–!3!years!is!more!than!temporary!(non-resident)!The!taxpayer!was!

considered!to!have!a!permanent!place!of!abode!outside!Australia!he!intended!to!

stay!with!his!family!in!Vila!for!3!years!at!least!and!then!further!extend!their!stay!

overseas.!He!was!considered!not!to!be!a!resident!despite!not!selling!his!Australian!

house!(though!attempts!were!made),!retaining!the!furniture!in!Australia,!receiving!

child!endowment,!and!having!to!return!after!18!months!due!to!illness.!!

&

&&&&&&&&*4$&).DD"//".0$%&.I&*+M+-".0N/&'"$B&

• Ruling!IT!2650!whether!a!taxpayer!has!a!“permanent!place!of!abode!outside!

Australia”.!Factors!include:!

–Intended!and!actual!length!of!stay!in!the!overseas!country;!

–Intentions!to!stay!in!the!overseas!country!permanently!or!temporarily;!

–Location!of!established!home;!

–Duration!and!continuity!of!taxpayer’s!presence!in!overseas!country;!

–Durability!of!Australian!associations!(eg,!place!of!education!of!taxpayer’s!children).!

!

D" !ED<'.1()$%)(

F9%)(G.)&%?1C(B(H(I(

a) An!individual!is!a!tax!resident!of!Australia!when!his!or!her!physical$presence!in!

Australia,!continuously!or!intermittently,!is!for!more$than$one-half$of$the$income!

year.!

b) Exceptions:!

i)!If!the!Commissioner!is!satisfied!that!the!individual’s$usual$place$of$abode$is$

outside$Australia;$and!

ii)!The!individual!does!not!intend!to!take!up!residence!in!Australia.!

•Working$holiday$visa$holder!who!was!in!Australia!for!more!than!183!days!was!not!a!

resident!as!their!“usual!place!of!abode!was!outside!Australia”:!

CL:!9$&F.5/-%5H&'&()*&(2015)!

~!Special!rules!apply!to!working!holiday!makers:!

Ø TR!98/17!-183!DAYS!&!intends!to!take!up!residence!in!Aus!

NOTE:!Domicile!–!PERMANENT!PLACE!

!!!!!!!!!!!183!day!test!–!USUAL!PLACE!

!

J" G92$+.,,9.)&/,()$%)(

• Applies!in!relation!to!Commonwealth!superannuation!funds.!

• Under!the!superannuation!test,!the!member!of!a!Commonwealth!superannuation!

fund!(ie,!Commonwealth!public!servants)!and!the!member’s!family!are!deemed!to!

be!tax!residents!of!Australia.!

!

!

Document Summary

General principles: a resident of australia for tax purposes will be taxed on income from all sources: See, s 6-5(2) itaa97: a foreign resident for tax purposes will be taxed on income from australian sources only: Differ depending on whether the individual tax payer is a resident for tax purposes or a foreign resident. Broadly, a foreign resident does not receive the benefit of the tax-free threshold: foreign residents : Do not have access to many personal tax offsets. When is a taxpayer a tax resident of australia: individuals s6(1) itaa36. Factors considered by the courts: time physically spent in australia. If the person is a visitor, the frequency, regularity and duration of visits: Cl: irc v lysaght [1928] - : one week each month in the uk, established a place of abode in ireland, had bank accounts in both uk & ireland.