BFC2140 Lecture Notes - Lecture 9: Squared Deviations From The Mean, Risk Premium, Standard Deviation

21 Oct 2018

School

Department

Course

Professor

Document Summary

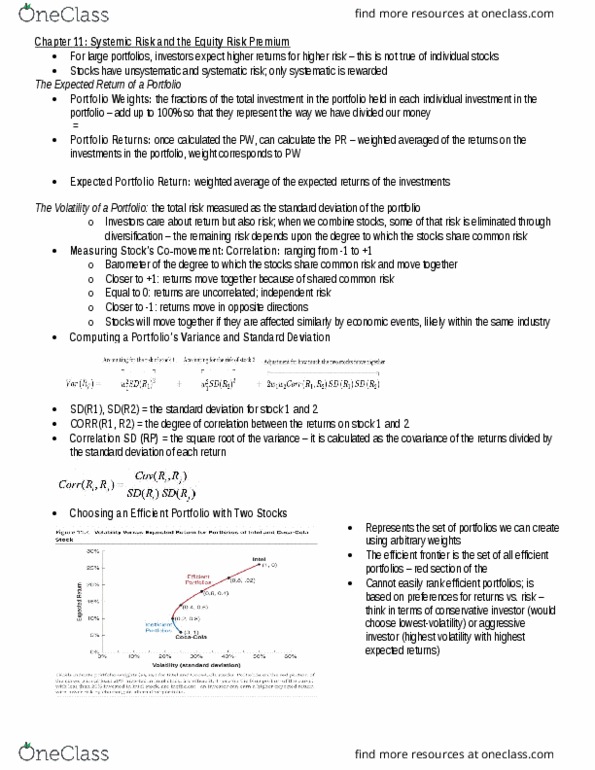

Understand how risk and return are defined and measured. Know how to calculate realised returns, holding period returns, average returns and standard deviation (volatility) for individual securities. Understand the importance of covariance and correlation between returns on assets in determining the risk of a portfolio. Understand how to calculate expected return (weighted average) and risk (standard deviation) for a portfolio consisting of 2 risk assets. Explain how diversified portfolios remove unsystematic risk, leaving systematic risk as the only risk requiring a premium. Chapter 11: risk and return in capital markets (p. 323-345) Standard deviation is the square root of the variance: coefficient of variation (cv) - standardised measure of dispersion about the expected return. Indicates how much risk we face per unit of return. If two securities have the same risk, then the one with higher return is preferable. If = +(cid:1005), (cid:374)o risk redu(cid:272)tio(cid:374) is possi(cid:271)le. If = -1, complete risk reduction is possible.