ACC1000 Lecture Notes - Lecture 16: Income Statement, Complete Control, Legal Personality

Document Summary

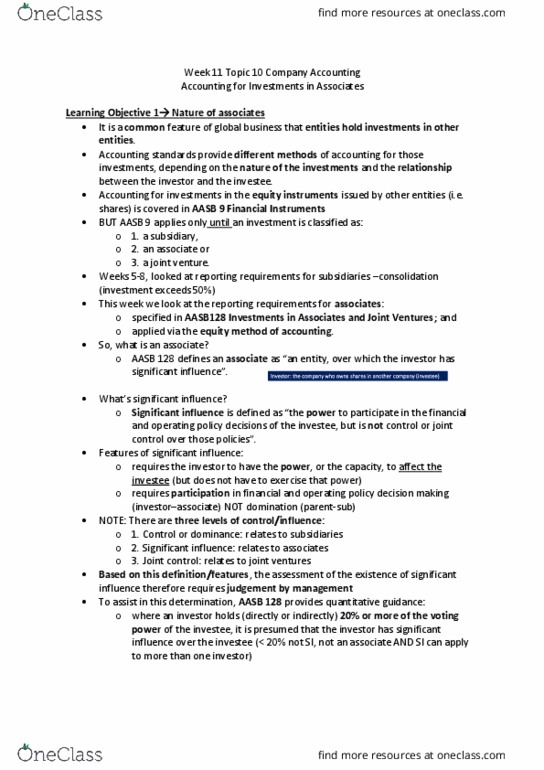

Objective (see acctg 102 for nz framework: improve the relevance, faithful representation, and comparability of the info that a reporting entity provides in it"s fs about a business combination and its e ects. To accomplish that, this nz ifrs establishes principles and requirements for how the acquirer: Recognises and measures in its fs the identi able assets acquired, the liabilities assumed, and any non- controlling interest in the acquiree; Recognises and measures a gain from a bargain purchase (opposite of goodwill) Determines what info to disclose to enable users to understand the nature and nancial e ects of the business combination. Parent" and the acquiree is called the subsidiary". Formation : parent forms new company, new company is therefore a subsidiary. Merger : new company is formed to buy the shares of two or more existing companies, therefore existing companies become subsidiaries (shares of new company are used as payment / exchanged for the old company"s shares)