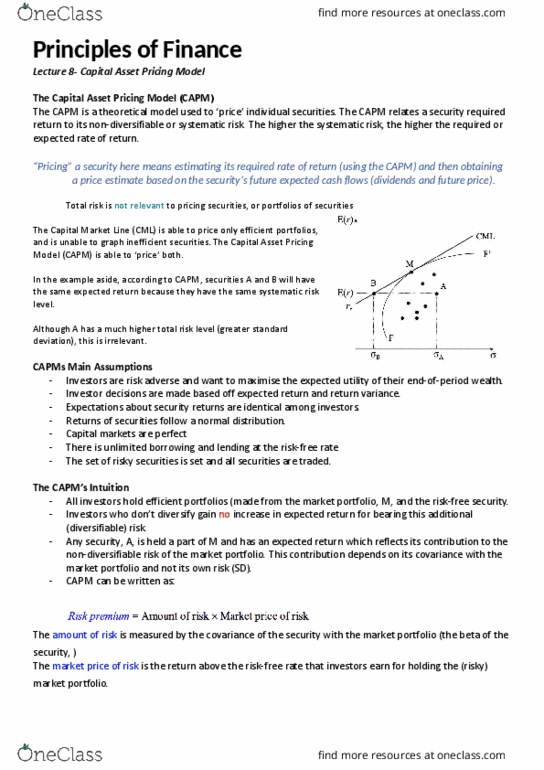

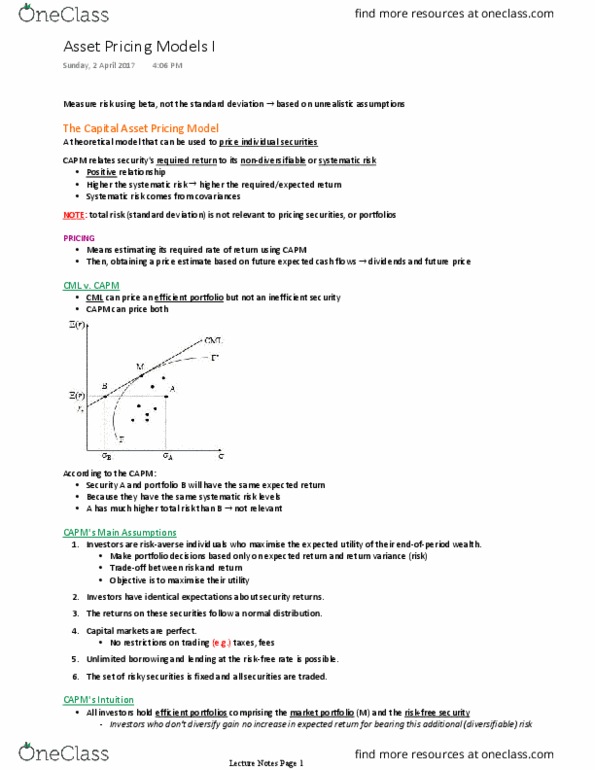

FNCE10002 Lecture Notes - Lecture 10: Dividend Payout Ratio, Australian Taxation Office, Capital Gains Tax

Document Summary

If the capm is valid, returns in the test period should be explained by the betas from the estimation period. If a (cid:272)o(cid:373)pa(cid:374)(cid:455) does(cid:374)"t pa(cid:455) di(cid:448)ide(cid:374)ds, (cid:455)ou (cid:272)a(cid:374) (cid:373)ake o(cid:374)e (cid:455)ou(cid:396)self: (cid:862)ho(cid:373)e-(cid:373)ade di(cid:448)ide(cid:374)ds(cid:863: suppose you own 100 shares, each with a market price of . If you wanted to, you could sell 5 shares (for : then you would have shares worth and in cash, this looks identical to case 1, explanation: a dividend is a partial liquidation of a company. To a first approximation, it does(cid:374)"t (cid:373)atte(cid:396) (cid:449)hethe(cid:396) pa(cid:396)tial li(cid:395)uidatio(cid:374) is u(cid:374)de(cid:396)take(cid:374) (cid:271)(cid:455): the company (paying a dividend), or, a shareholder (selling some shares) In practice, there are three differences between cases 1 and 2. These are: transaction costs, voting rights, taxes, transaction costs. In case 1 there are transaction costs in paying a dividend (e. g. postage, bank fees) In case 2 there are transaction costs like brokerage. But this difference is usually very small: voting rights.