ACCT10002 Lecture Notes - Lecture 7: Accounts Payable, Annual Leave, Promissory Note

Introduction to Financial Accounting Wk. 7

CHAPTER 9: REPORTING AND ANALYSING LIABILITIES

Current liability: an obligation that can reasonably be expected to be paid within 1 year or

within the operating cycle

Legal obligation: an obligation that derives from:

• A contract( through explicit/implicit terms)

• Legislation, or

• Other law

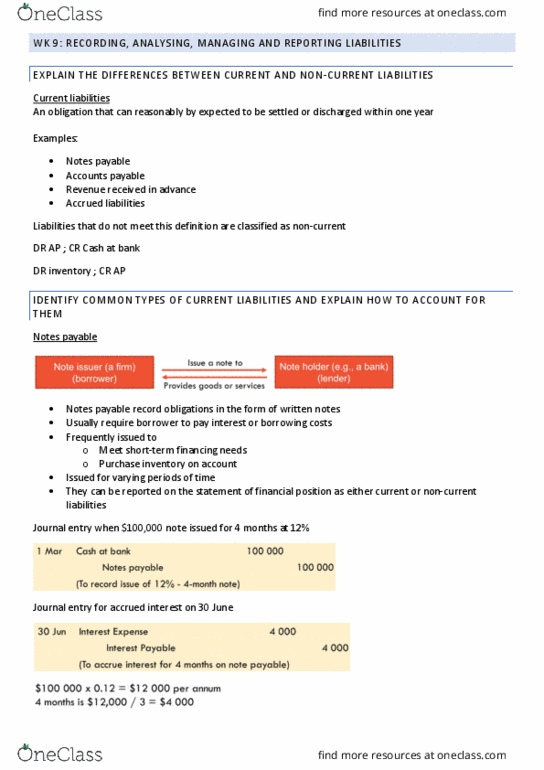

Notes payable: obligations in the form of written promissory notes

• When purchasing inventory on credit, notes payable sometimes used instead of

accounts payable because they give lender written documentation of obligation in

case legal avenues are needed to collect the dent

• Usually require borrower to pay interest and frequently issued to meet short-term

financing needs

Interest: a cost of borrowing money

• Also called borrowing costs or finance costs

Face value: principal payable at maturity

Eg.

Cash DR

Notes Payable CR

Notes Payable

Interest Payable

Cash

Payroll and Payroll Deductions Payable

• Employers incur liabilities relating to salaries and wages

• Employer deducts amounts from employees wages:

o if required to deduct tax from gross pay and pass to ATO

o deductions paid to medical funds/health insurance

o trade units on behalf of employees

• until these deductions, such as pay-as-you-go (PAYG) withheld tax, are remitted to

appropriate parties, they are recorded as increases to appropriate liability accounts

• tax authorities have fines and penalties in employers if taxes aren’t calculated

correctly and paid on time

Salaries and Wages Expense 100 000

Pay-as-you-go withheld tax payable 32 036

Salaries and wages payable 67 964

(to record payroll and withheld taxes for the week ending 7 March)

Salaries and wages payable 67 964

Cash 67 964

(to record payment of taxes for March 7 payroll)

Pay-as-you-go withheld tax payable 32 036

Cash 32 036

(to record payment of withheld taxes remitted to Taxation office for March 7 payroll)

Other payroll deductions

• private health insurance

• superannuation contributions (these are required by law)

o aim is to provide employees with a lump sum and/or regular payments on

retirement

• Union fees

• Charity donations

• Payroll liability accounts are classified as CL; must be paid to employees or remitted

to tax authorities & other parties in short term

Salaries and Wages Expense 37 000

Pay-as-you-go withheld tax payable 32 000

Superannuation payable 4000

Union fees payable 1 00

(to record withheld taxes and deductions for the week ending 7 March)

Employers may also have other costs relating to employees:

• Annual leave

• Workers compensation: an insurance scheme to compensate employees for injuries

or death at work

• Parental leave

• Sick leave

• Long service leave: generally granted after 10 years of service but only accrued after

employees have completed after a number of years of service

o May have CL (for portion to be paid within less than a year) and NCL

component (amount to be paid after one year)

Some are required by law, or specified in salary and wage awards and contracts

• Employees usually entitled to number of paid weeks and annual leave and a number

of days of sick leave

• As employees only become entitled to these benefits pro-rata as they work

throughout the year, employer usually accrues liability at regular intervals

• Workers compensation is usually paid as a yearly premium

Revenues Received in Advance

How entities account for revenues received in advance:

1. When advance is received, cash is increased and CL identifying source of revenue

received in advance is also increased

2. When service is performed, revenue received in advance account is debited and

revenue is increased

Satisfied when 5-step process of revenue recognition is complete

NON-CURRENT LIABILITIES

Non-current liabilities: obligations that are expected to be paid after 1 year or outside

normal operating cycle

• Often bank loans or long-term notes

Public companies may raise debt finance from public in form of:

• Notes issued in small denominations (usually $1000 or multiples of it)

Unsecured notes: notes not subject to a security over assets of the issuing company

Debentures: notes subject to a secured charge over some of the issuer’s assets

“security over assets”: a right to have the assets liquidated to recover unpaid amounts of

debt if the debtor defaults on payment

Convertible notes: notes able to be converted into shares instead of being repaid at

maturity

Why businesses issue unsecured notes or debentures (debt financing)

1. Shareholder control isn’t affected: note holders don’t have voting rights, so current

shareholders retain full control

2. Tax savings result: interest is deductible for tax purposes; dividends aren’t

3. Earnings per share may be higher: although interest expense reduces profit, EPS

often higher with debt financing because no additional shares are issued

Disadvantage to debt financing

• Company locks in fixed payments that must be made in good times and bad

• Interest must be paid on a periodic basis

• Principal (face value) of notes must be paid at maturity

• Of profit target not achieve, ROE can be low/negative

Company with fluctuating earnings and weak cash position may have trouble paying interest

in periods of low earnings. Might lead to bankruptcy

With equity: company can decide low or no dividends during times of low earnings

DETERMINING MARKET VALUE OF UNSECURED NOTES AND DEBENTURES

Issue price: amount paid for note by investor/lender at time of issue

Market value: price at which note is traded by willing parties

Contract interest rate: rate used to determine the amount of interest the borrower pays

and investor receives

• Usually stated as an annual interest rate

• Interest usually paid half yearly

Market value may differ from face value of note

Present value: equivalent value today

Market interest rate: the rate investors demand for lending funds to the entity

Discounting: the process of finding the present value

Document Summary

Current liability: an obligation that can reasonably be expected to be paid within 1 year or within the operating cycle. Legal obligation: an obligation that derives from: a contract( through explicit/implicit terms, legislation, or, other law. Interest: a cost of borrowing money: also called borrowing costs or finance costs. Salaries and wages payable (to record payment of taxes for march 7 payroll) Salaries and wages payable (to record payroll and withheld taxes for the week ending 7 march) Pay-as-you-go withheld tax payable (to record payment of withheld taxes remitted to taxation office for march 7 payroll) Union fees payable (to record withheld taxes and deductions for the week ending 7 march) Employers may also have other costs relating to employees: Satisfied when 5-step process of revenue recognition is complete. Non-current liabilities: obligations that are expected to be paid after 1 year or outside normal operating cycle: often bank loans or long-term notes.