ACCG100 Lecture Notes - Lecture 3: Accounting Equation, Accounts Receivable, Deferral

14 Sep 2018

School

Department

Course

Professor

Document Summary

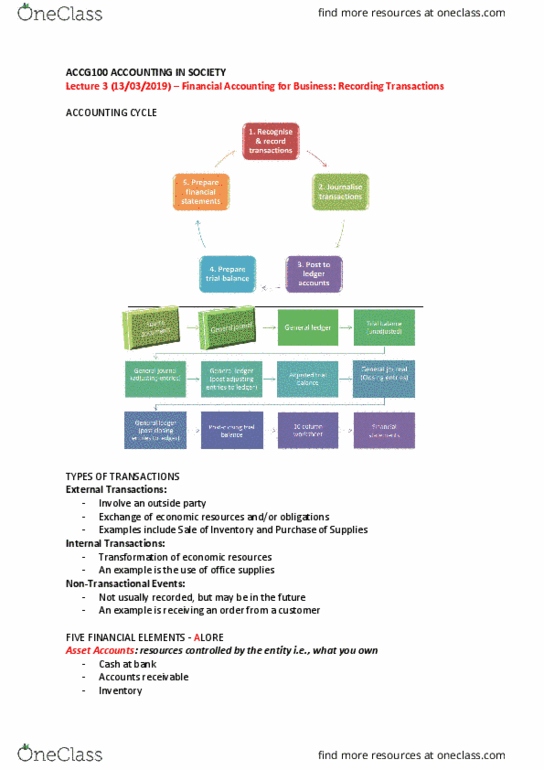

Examples include sale of inventory and purchase of supplies. An example is the use of office supplies. Not usually recorded, but may be in the future. An example is receiving an order from a customer. Asset accounts: resources controlled by the entity i. e. , what you own. Assets: resources controlled by the entity as a result of past transactions or events from which future economic benefits are expected to flow to the entity. Liability accounts: future sacrifices of economic benefits i. e. what you owe. Liabilities: present obligations of an entity arising from past transactions or events, the settlement of which is expected to result in an outflow of resources from the entity. Equity accounts: claims of owners i. e. what is left of what you own after deducting what you owe. Capital (cid:894)the ow(cid:374)er share of the (cid:271)usi(cid:374)ess, i. e. ow(cid:374)er(cid:859)s (cid:272)apital(cid:895) Drawings are what the owners take out from the business for their personal use.