BU1002 Lecture Notes - Lecture 10: Budget, Strategic Planning, Human Resource Management

14 Jun 2018

School

Department

Course

Professor

Budgeting and Strategic Planning

• Strategic planning longer term planning (typically, 3-5 years)

• It is usually carried out by senior management

• It commonly related to broader issues such as business takeovers, expansion plans, deletion

of business segments and radical product/service development

• Budgeting is a process that focuses on short term

• Budgets operationalise strategic plans and allow operation areas to understand how their

area contributes to the entity's strategic objectives

Budgets

• A budget is the quantitative expression of an entity's plans

• Entities engage in a planning process that requires involvement in a budgeting process

• Part of the formal planning process relates to an entity's operational plans, including short

term goals and targets

• Performance management involves setting targets in other than just financial terms

o E.g. improving customer service, corporate governance, management techniques

and human resource management

• Budgeting can assist in decision making by:

o Putting into operation longer term plans

o Setting targets for managers

o Identifying resource constraints in budget period

o Identifying periods of expected cash shortages and excess cash holdings

o Assisting and short-term planning decisions, such as capacity utilisation

o Providing profit forecasts and other financial data to capital markets

o Forecasting data such as sales or fees which commonly set the level of activity for

the budget period

o Helping determine required inventory levels and purchasing requirements for raw

materials

o Planning labour and other inputs the other inputs

find more resources at oneclass.com

find more resources at oneclass.com

o Determining the ability of entity of meeting financial commitments

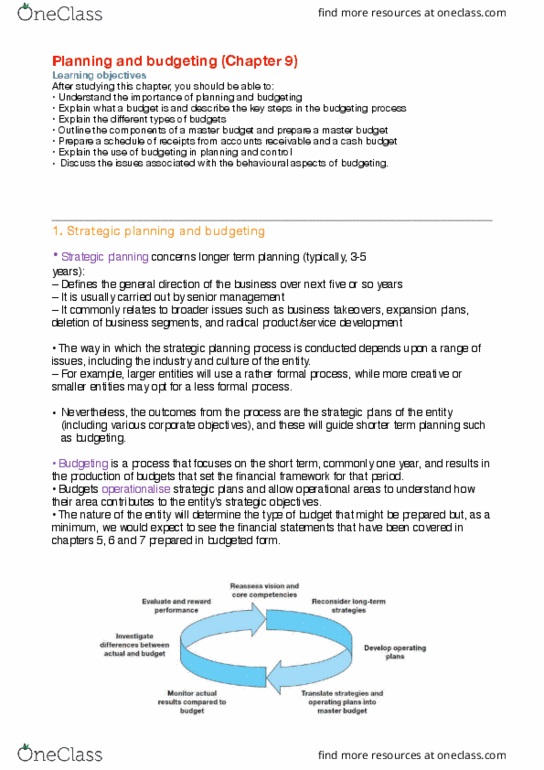

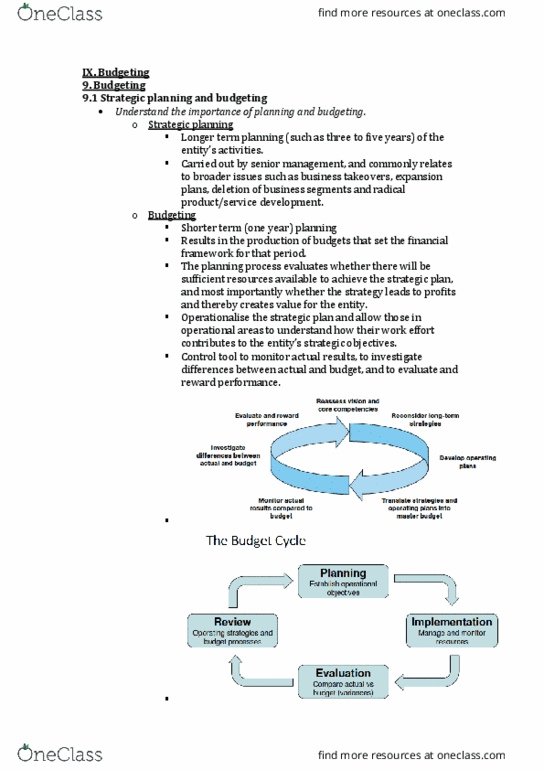

The Budgeting Process

1. Consideration of past performance

2. Assessment of expected trading and operating conditions

3. Preparation of initial budget estimates

4. Adjustment to estimates based on communication with, and feedback from managers

5. Preparation of budgeted reports and sub-budgets

6. Monitoring of actual performance against the budget over the budget period

7. Making any neccesary adjustments to the budget during the budget period

The budgeting process

• Throughout the process, communication with managers who are affected by the budgets

should occur

• Simons '3 wheels of planning' highlights the need for those within the entity to work

together to develop the profit plan for the coming year

• The interaction of the various personaell enable them to understand the impact of their

decisions and to acess whether the value is created for the entity

Types of Budgets

• Sales (or fees) budget

• Production and inventory budgets

• Purchases budget

• Manufacturing overhead budget

• Program budget

• Budgeted income statement

• Budgeted balance sheet

• Capital budgets

• Cash Budgets

Master Budget

• A master budget is a set of interrelated budgets for a future period which provides a

framework for viewing relevant budgets of an entity

• To enable the budget to be used as a control tool to monitor the entity's achievement of its

plans, classification of items included in the masters budget needs to mirror the entity's chart

of accounts

• Because budgets are based on forecasts about the future complete accuracy is impossible

and variances with inevitably arise

Stages in preparation of master budget

Service entity

• Determine the expected level of activity for the budgeted period

• Developing the sales budget

• Developing a labour budget

• Developing an operating expenses budget

• Preparing a budgeted income statement

Manufacturing entity

• Determine the expected level of activity for the budgeted period

find more resources at oneclass.com

find more resources at oneclass.com

• Developing the sales budget

• Developing a production budget

• Developing a materials budget

• Labour budget

• Overhead budget

• Developing a selling and administrative expense budget

Budget examples

• Budgets form part of management accounting

• Not bound by regulatory requirements

• The info generated is based on users needs for decision making

• Prepared budgets can be interrelated - i.e. production budget - units produced will also

impact on the labour and materials budget

Cash Budget

• The cash budget is a statement of expected future cash receipts and payments

• Best prepared on a month by month basis to enable closer monitoring of cash position

• It assist decision making by

o Documenting timing of all cash receipts and payments

o Helping to identify periods of expected cash shortages and surpluses

o Identifying suitable times for purchase of non-current assets

o Assisting with planning and use of borrowed funds

o Providing framework for 'what if' analysis

• For an entity that provides goods or services on credit, one of the main tasks in the

preparation of a cash budget is calculating the cash receipts from the credit sales or fees

generated

• Need to look at past experience to identify timing patterns of receipts from customers

• This is commonly shown in a schedule of receipts from debtors / accounts receivable

• Also necessary to identify cash payments to suppliers and various expenses

Preparation of a Cash Budget

1. Assess the trading and operating conditions and gather necessary information

2. Prepare initial budget estimates

3. Prepare a schedule of receipts and other sub-budgets

Schedule of Receipts

Step 1: Access the trading and operating conditions and gather necessary information

Trading information:

Experience shows debtors settle accounts in the following pattern

• 50% in the month following sale

• 40% in the second month following sale

• 10% in the third month following sale

Actual Sales

• October $210,000

• November $282,00

• December $303,000

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Strategic planning longer term planning (typically, 3-5 years) It is usually carried out by senior management. It commonly related to broader issues such as business takeovers, expansion plans, deletion of business segments and radical product/service development. Budgeting is a process that focuses on short term. Budgets operationalise strategic plans and allow operation areas to understand how their area contributes to the entity"s strategic objectives. A budget is the quantitative expression of an entity"s plans. Entities engage in a planning process that requires involvement in a budgeting process. Part of the formal planning process relates to an entity"s operational plans, including short term goals and targets. Performance management involves setting targets in other than just financial terms. E. g. improving customer service, corporate governance, management techniques and human resource management. Identifying periods of expected cash shortages and excess cash holdings. Assisting and short-term planning decisions, such as capacity utilisation. Providing profit forecasts and other financial data to capital markets.