MAA103 Lecture Notes - Lecture 5: Harvey Norman, Cash Flow, Income Statement

Document Summary

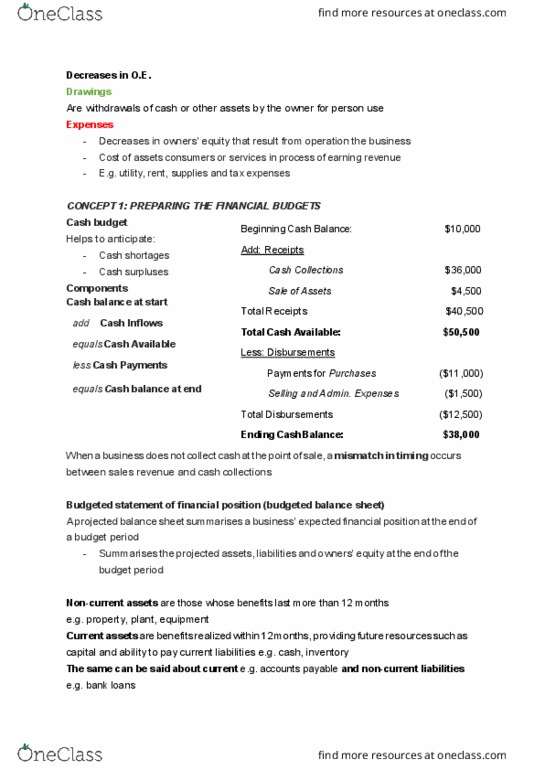

Statement that shows the expected revenues and planned expenses of the firm and arrives at profit projections. Intuitively, we want to forecast how much profit/loss we intend to make within the budgeted period. The data from this should flow on from the sales budget, cost of sales budget and expenses budget. Fo(cid:396) a (cid:272)o(cid:373)pa(cid:374)(cid:455)"s ta(cid:454) e(cid:454)pe(cid:374)ses (cid:455)ou (cid:272)a(cid:374) use 30%, do(cid:374)"t (cid:374)e(cid:272)essa(cid:396)il(cid:455) ha(cid:448)e to (cid:449)o(cid:396)(cid:396)(cid:455) a(cid:271)out it fo(cid:396) partnership. Records how much cash we have at the end of the budgeted period. Shows expected cash receipts and payments, a(cid:374)d ho(cid:449) the(cid:455) affe(cid:272)t the (cid:271)usi(cid:374)ess"s (cid:272)ash (cid:271)ala(cid:374)(cid:272)e. this helps the o(cid:449)(cid:374)e(cid:396)s a(cid:374)ti(cid:272)ipate cash shortages, or cash excesses that could be better used for profitable projects or investments. *cash = part of working capital e. g. budget period. *cash collections: quite often a business might not actually collect all the cash at the point of sale.