MAA103 Lecture Notes - Lecture 8: Office Supplies, Income Statement, Net Profit

26 Jul 2018

School

Department

Course

Professor

Document Summary

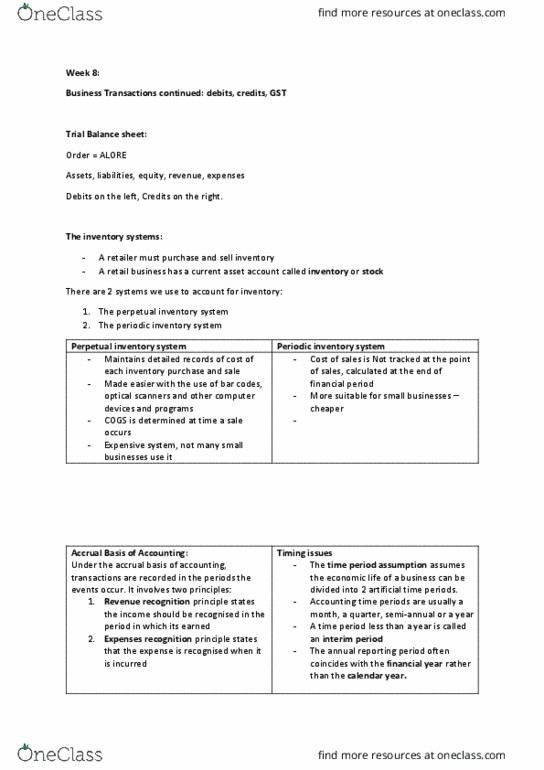

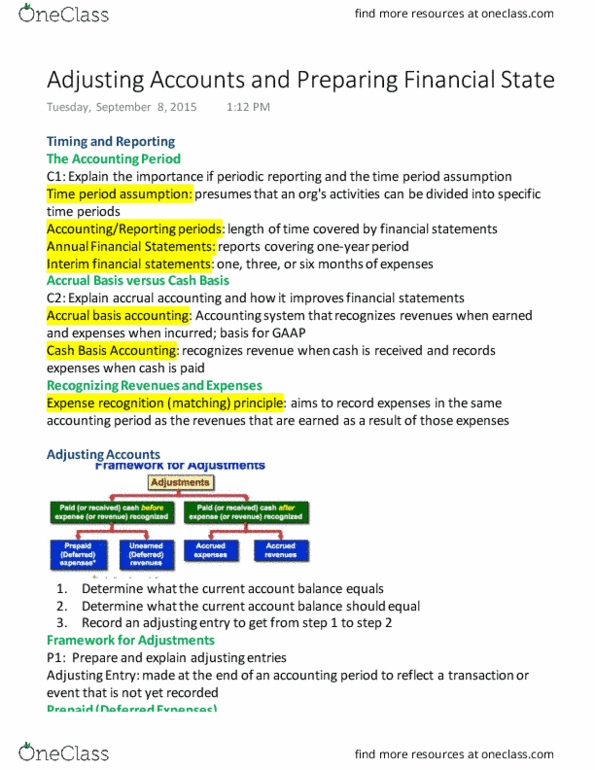

Topic 8 - balance day adjustments and preparation of classified accounting reports. The accounting time period assumption assumes the economic life of a business can be divided into artificial time periods. Accounting time periods are usually a month, a quarter, semi-annual or a year. A time period less than a year is called an interim period. The annual reporting period often coincides with the financial year rather than the calendar year. Under the accrual basis of accounting, transactions are recorded in the periods the events occur. Revenue recognition principle states the income should be recognised in the period in which it is earned. Expense recognition principle states that the expense is recognised when it is incurred. Balance day adjustments are adjustments that need to be made on the relevant accounts at the end of the financial period. Balance day adjustments are required to ensure that. Revenues are recorded in the period they are earned.