MAA103 Lecture Notes - Lecture 7: Capital Account, Trial Balance, General Ledger

25 Jul 2018

School

Department

Course

Professor

Document Summary

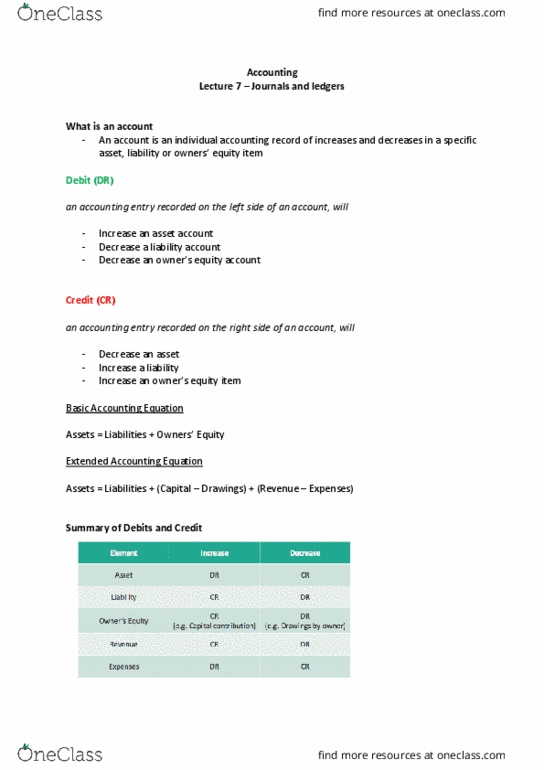

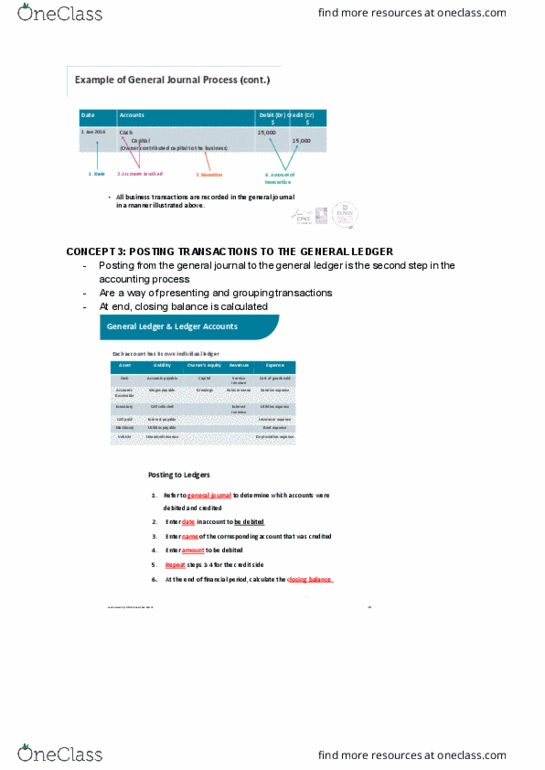

Topic 7 - transaction analysis: the recording process. An account is an individual accounting record of increases and decreases in a specific asset, liability or owner"s equity item. Examples: cash, accounts payable, capital, service revenue, wages expense etc. Is always an accounting entry recorded on the left side of a t-account. Is always an accounting entry recorded on the right side of a t-account. Basic accounting equation: a = l + oe. A = l + capital + revenue drawings expenses. A + d + e = l + c + r. The first step in the process of preparing a journal entry is to analyze the accounts involved in a business transaction. Apply the rules of debit and credit based on the type of each account. The total amount debited and credited should always be equal, thereby ensuring the accounting equation is maintained.