MAA103 Lecture Notes - Lecture 4: Income Statement, Target Costing, Cash Flow Statement

25 Jul 2018

School

Department

Course

Professor

Document Summary

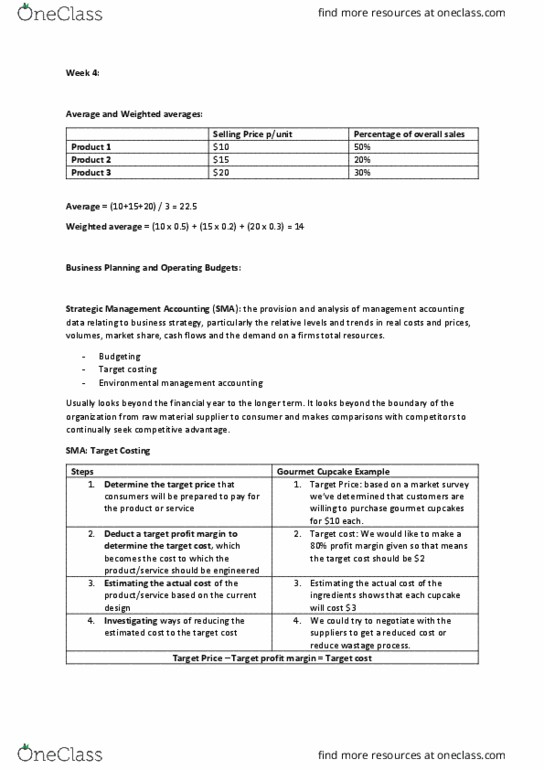

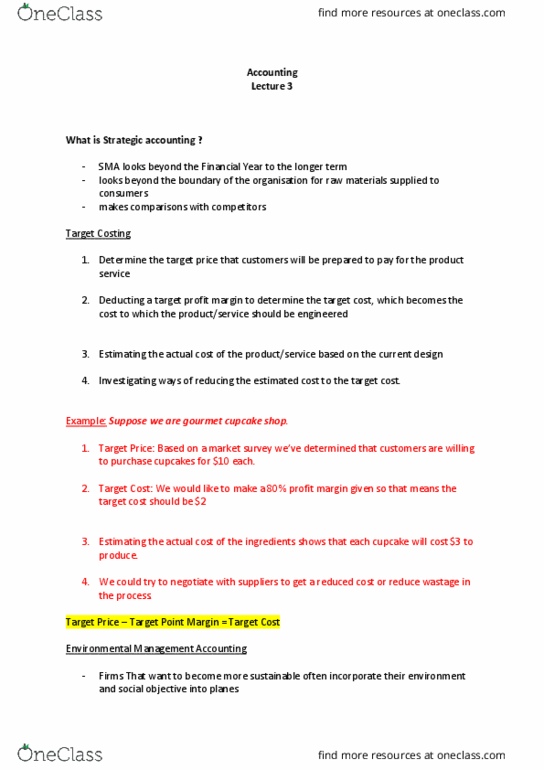

Topic 4 - business planning and operating budgets. Strategic management accounting is the provision and analysis of management accounting data relating to: business strategy trends in real costs, prices and volumes market share cash flows and the demand on a firm"s total resources. Strategic management accounting (sma) looks beyond the financial year to the longer term. Sma looks beyond the boundary of the organisation from raw material supplier to consumer. Sma makes comparisons with competitors to continually seek competitive advantage. Target costing is concerned with managing whole-of-life costs during the design phase of the product life cycle and involves four stages: Determine the target price that customers will be prepared to pay for the product service. Deducting a target profit margin to determine the target cost, which becomes the cost to which the product/service should be engineered. Estimating the actual cost of the product/service based on the current design. Investigating ways of reducing the estimated cost to the target cost.