MIS171 Lecture Notes - Lecture 7: Exponential Smoothing, Time Series, Nonlinear Regression

8 Sep 2018

School

Department

Course

Professor

Document Summary

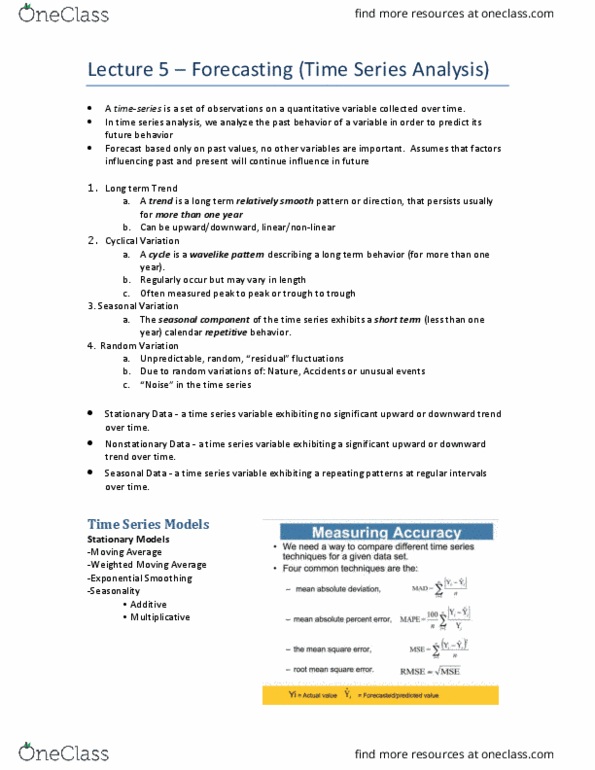

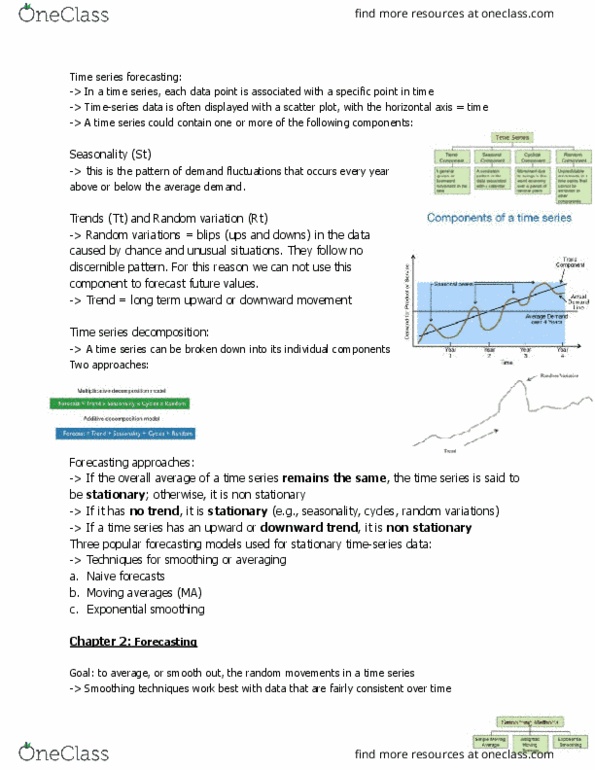

Is usually done to help us better see patterns, helps if out the irregular the time series data to you (cid:862)s(cid:373)ooth(cid:863) help answer this question. A time series plot should help you to answer this question. For seasonal data, we might smooth out the seasonality so that we can identify the trend. L-period moving average the average of the l data points. For a 5 year moving average, l = 5. For a 7 year moving average, l = 7. A bit of difficulty when there are even number of periods. Example: five-year moving average for computing means) roughness to (length of. Single exponential smoothing model irregular components gi(cid:448)es (cid:373)ore s(cid:373)oothi(cid:374)g, larger gives less smoothing for smoothing out unwanted cyclical. The forecast error or residual is the difference between the actual value in time t and the forecast value in time t. Measures of match the actual values. gauge how well are used to fit the forecasts.